EU CBAM for UK Exporters: The Executive Guide for British Manufacturers Selling into Europe (2026–2027)

- Ahtesham Shaikh

- 1 hour ago

- 16 min read

CBAM Journal Research & Intelligence Team. See our Editorial Standards and AI Usage Disclosure for how this report was produced and verified — Sekason Research Limited, London

Section 1: Executive Summary

UK manufacturers exporting to the EU face commercial exposure with no direct legal basis. The EU CBAM definitive regime entered into force on 1 January 2026; from that date, the legal duty to buy and surrender CBAM certificates sits with the EU importer, not the UK exporter. That legal separation offers no commercial protection: EU buyers now need verified embedded-emissions data to manage their own certificate costs, and a UK manufacturer that cannot supply it credibly risks losing preferred-supplier status before a single euro of tax is calculated.

Key Findings at a Glance

Finding | Implication for UK Exporter |

EU CBAM definitive regime live from 1 January 2026 | EU customers are now actively requesting embedded-emissions data |

Legal certificate obligation sits with the EU importer, not the exporter | UK exporters have no direct EU CBAM tax liability, but face commercial pressure regardless |

UK CBAM enters force 1 January 2027 (Finance Act 2026) | UK exporters selling into the EU may separately become UK importers if they bring CBAM-scope goods into the UK — dual-regime exposure is possible |

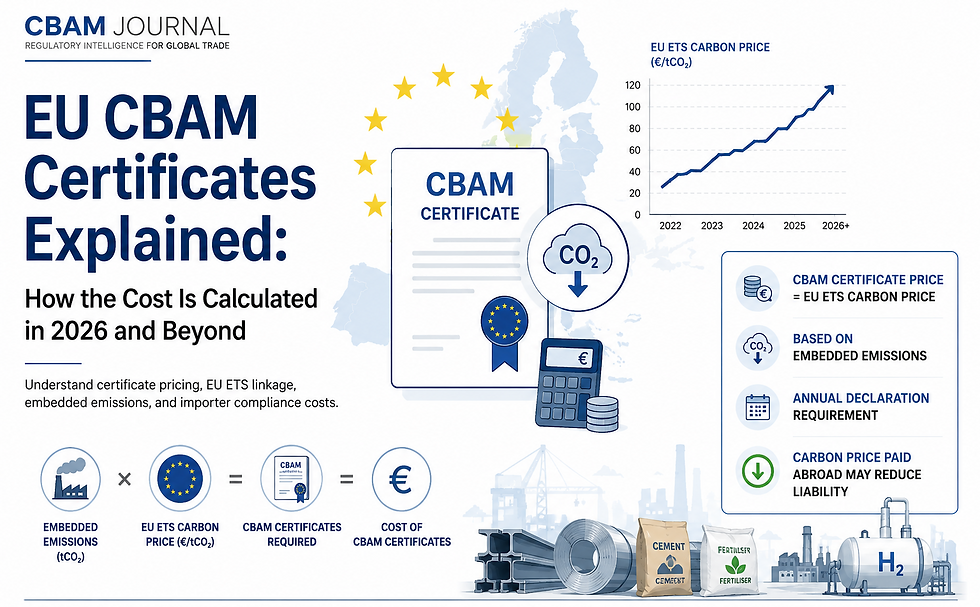

No single fixed EU or UK per-tonne CBAM price is published in primary legal sources | Financial exposure must be modelled against the prevailing EU ETS price at the time of certificate purchase — no fixed CBAM tariff exists in EU or UK primary legislation. |

UK CBAM registration window expected to open late 2026 | Businesses trading in both directions should track UK registration in parallel with EU customer readiness |

Five Immediate Priorities for UK Exporters

Identify every EU customer receiving CBAM-in-scope goods (iron & steel, aluminium, cement, fertilisers, hydrogen) and confirm which has already made a formal data request.

Assign a single internal owner for CBAM data — this cannot sit informally across sales and production without slippage.

Prepare an embedded-emissions evidence pack per installation, not per shipment — EU declarants will ask repeatedly, not once.

Track the UK CBAM registration window (expected late 2026) even where primary exposure today is EU-side — many exporters will also be UK importers of intermediate goods.

Do not quote a fixed CBAM cost to customers or in contracts. No authoritative fixed tariff exists in EU or UK primary legislation — exposure is a function of the prevailing EU ETS price and declared emissions, not a set number.

Executive Decision Snapshot

Question | Answer |

Am I legally liable for EU CBAM? | No — the authorised EU importer is the legal declarant |

Am I commercially exposed? | Yes — customer data requests, procurement decisions and contract terms depend on your emissions evidence |

Do I have a UK CBAM obligation? | Not yet — applies from 1 January 2027; relevant if you import CBAM goods into the UK |

What should I do in the next 90 days? | Build the evidence pack and governance structure set out in Section 7 |

This report does not explain EU CBAM as legislation in isolation. It explains what the definitive regime means operationally for a UK manufacturer answering a customer's emissions questionnaire this quarter, not next year.

Section 2: Regulatory Context

Understanding the EU CBAM Definitive Regime

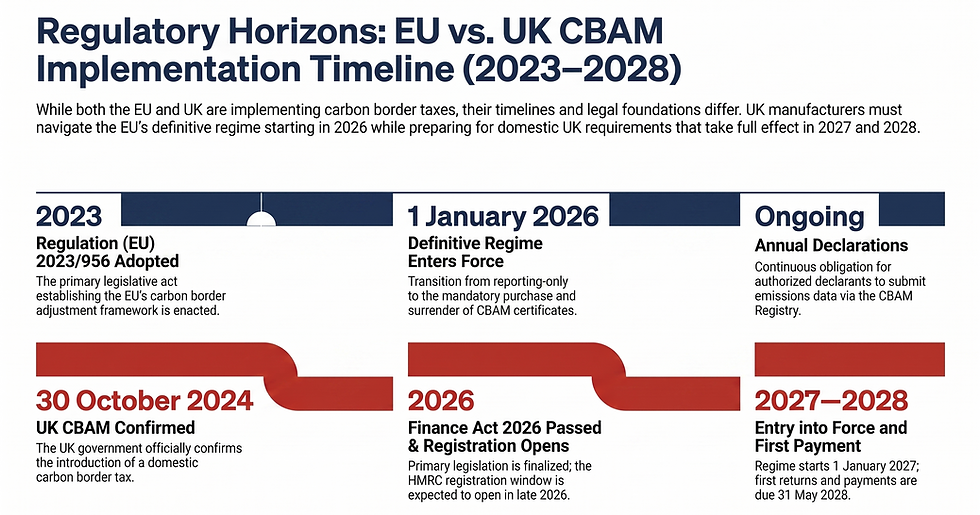

The EU Commission's definitive regime for CBAM began on 1 January 2026, replacing the earlier transitional reporting-only phase with a system in which authorised declarants must purchase and surrender CBAM certificates against the embedded emissions of imported goods. The underlying instrument is Regulation (EU) 2023/956, with implementing detail set out through TAXUD guidance and the CBAM Registry infrastructure.

For a UK exporter, the practical consequence is not a new form to file — it is a new question the customer starts asking. Before 2026, EU importers largely absorbed CBAM as a reporting exercise with limited financial consequence. From 1 January 2026, every certificate an importer must buy is priced against real embedded emissions, which means the accuracy and availability of a UK supplier's emissions data now has a direct line to the importer's cost base.

The EU importer remains the legal declarant throughout. What has changed is that the importer's ability to comply cheaply and accurately now depends on the quality of data the UK exporter can produce. This is the commercial mechanism driving customer behaviour — not a change in UK exporters' legal status.

Who Is Legally Responsible?

Party | Legal Position Under EU CBAM |

EU Importer | Legal declarant; purchases and surrenders CBAM certificates |

Authorised CBAM Declarant | The registered entity submitting annual declarations via the CBAM Registry |

UK Manufacturer | No direct legal obligation under EU CBAM; commercial obligation to supply data flows from customer contracts, not statute |

Exporter | Same position as manufacturer where distinct from the producing entity |

Installation Operator | Relevant to the registry-based evidence chain connecting exporters to EU declarants. Registry functionality enabling non-EU installation operators to upload emissions data directly is an evolving part of the CBAM Registry infrastructure; exporters should confirm current functionality directly with TAXUD before relying on it as a compliance channel. |

The distinction that trips up most UK exporters: legal liability and commercial obligation are not the same thing. You can be entirely correct that "CBAM isn't my law" while still losing a contract because you couldn't produce the data your customer's law requires them to have. Compliance managers should treat this as a customer-relationship question, not a legal one.

What Changed on 1 January 2026?

Three structural shifts define the move from transitional to definitive regime:

Certificates replace quarterly reporting. Importers now purchase CBAM certificates tied to embedded emissions rather than simply filing quarterly emissions reports.

Financial obligations are linked to EU ETS prices. Certificate cost is not fixed — it tracks the prevailing EU ETS carbon price, multiplied by declared embedded emissions. multiplied by declared embedded emissions. No single fixed per-tonne certificate price appears in EU primary legislation; any quoted static CBAM cost figure should be treated as illustrative, not authoritative, and verified against the prevailing EU ETS price.

Annual declarations and registry requirements formalise the data chain. The CBAM Registry is now the operational backbone connecting installation operators, exporters and importers.

Certificate cost became a live financial line item tied to real emissions data in January 2026. That gave EU procurement teams a direct financial reason to interrogate supplier emissions claims — something the reporting-only regime never forced them to do.

Table — Transition Phase vs Definitive Phase

Feature | Transitional Phase (pre-2026) | Definitive Phase (from 1 Jan 2026) |

Obligation type | Quarterly reporting only | Certificate purchase and surrender |

Financial consequence for importer | Minimal/none | Directly tied to EU ETS price × embedded emissions |

Exporter data pressure | Low | High — data quality now affects importer cost |

Registry role | Reporting portal | Active certificate and evidence infrastructure |

Table — Legal vs Commercial Responsibility

Responsibility | Legal (EU CBAM Statute) | Commercial (Customer Relationship) |

Certificate purchase | EU importer | N/A |

Emissions data provision | Not mandated by UK exporter's home jurisdiction | A frequent condition of contract or procurement approval |

Verification | Importer's declaration is legally binding | Exporter's evidence quality determines commercial trust |

Section 3: Compliance Obligations

What UK Manufacturers Must Provide

EU customers are converging on a broadly consistent data request, even though no single legal instrument specifies exactly what a UK exporter must hand over. In practice, the request typically covers:

Embedded emissions at product and installation level

Production process descriptions, sufficient to support the emissions methodology used

Installation information — identifying the specific site of manufacture

Verification evidence supporting the emissions figures provided

Supporting documentation — energy source mix, production volumes, relevant certifications

Product-level emissions data, broken down where the customer's declaration requires product-specific figures rather than site averages

A complete evidence pack means the exporter can answer a data request without an ad hoc scramble — every element above exists in a standing, updateable file before the request arrives.

Responding to Customer Data Requests

A defined workflow addresses the two most common failure modes: slow first response, and inconsistent answers when different customers ask the same underlying question in different ways.

Customer Request Workflow

Stage | Action | Owner |

1. Receipt | Log the request centrally — do not let it sit in an individual sales inbox | Export Sales |

2. Internal data collection | Pull from the standing evidence pack, not from scratch | Production / Sustainability |

3. Quality assurance | Cross-check figures against the last verified submission to a different customer | Sustainability / Finance |

4. Submission | Respond within an agreed internal SLA | Export Sales |

5. Follow-up handling | Route methodology questions to whoever built the emissions calculation, not to sales | Production / Sustainability |

6. Documentation | File the exchange in the evidence pack for the next request | Operations |

Most existing guidance describes this as a legal reporting exercise and treats it nowhere as an operational process with owners, timelines and a paper trail. That gap is where SMEs lose time and credibility.

Internal Governance

CBAM data requests fail inside SMEs not because the data doesn't exist, but because no single person owns pulling it together under time pressure.

RACI Governance Matrix

Function | Role in CBAM Data Requests |

Senior Management | Accountable for CBAM readiness as a commercial risk, not a compliance footnote |

Operations | Responsible for maintaining installation-level production data |

Production | Responsible for process data feeding emissions calculations |

Finance | Consulted — models commercial exposure and contract risk |

Sustainability | Responsible for emissions methodology and verification evidence |

Export Sales | Responsible for first response and customer communication |

Legal | Consulted — reviews contract clauses referencing CBAM data obligations |

Required Documentation Checklist

Installation-level embedded emissions calculation

Verification records or third-party evidence supporting the calculation

Production process documentation

Energy source and mix data

Prior customer submissions (for consistency checking)

Registry upload records, where applicable

Evidence Retention Framework: Retain every version of emissions data submitted to any customer, with the date and methodology version used. Inconsistent figures across customers are the fastest way to trigger a challenge — see Section 9, FAQ 5.

Section 4: Key Dates and Deadlines

EU CBAM Timeline

Date | Milestone |

Pre-2026 | Transitional reporting-only phase |

1 January 2026 | EU CBAM definitive regime enters into force — certificate purchase and surrender obligations apply to authorised declarants |

Ongoing from 2026 | Annual declaration cycles and continuing registry-based evidence exchange |

UK Regulatory Milestones

Date | Milestone |

30 October 2024 | UK government confirmed UK CBAM would be introduced from 1 January 2027 |

2026 (Finance Act 2026) | Primary legislation establishing the UK CBAM charge, empowering secondary legislation |

Late 2026 (expected) | UK CBAM registration window expected to open |

1 January 2027 | UK CBAM enters into force; first accounting period is calendar year 2027 |

31 May 2028 | First UK CBAM return and payment due, covering the 2027 accounting period |

Table — EU vs UK Milestone Comparison

Milestone | EU CBAM | UK CBAM |

Regime start | 1 January 2026 | 1 January 2027 |

Legal basis | Regulation (EU) 2023/956 | Finance Act 2026 |

Registration opens | Already operational (Registry) | Expected late 2026 |

First accounting period | Ongoing from 2026 | Calendar year 2027 |

First return/payment | N/A (certificate purchase is continuous) | 31 May 2028 |

Executive Compliance Calendar: UK exporters selling into the EU should treat 2026 as the year customer data pressure intensifies, and late 2026 through mid-2027 as the window in which their own UK CBAM registration and readiness must be built in parallel, where relevant.

HMRC has not yet confirmed an exact registration opening date beyond the indicative late 2026 window; treat this timing as provisional until HMRC publishes a fixed date.

Section 5: Financial Exposure and Risk

Understanding Carbon Cost Exposure

CBAM certificate cost under the EU definitive regime is calculated as the prevailing EU ETS carbon price multiplied by the declared embedded emissions of the imported goods. Neither the European Commission nor TAXUD guidance publishes a single fixed per-tonne CBAM price in primary legal text. Cost exposure moves with the EU ETS market; any static per-tonne figure quoted elsewhere should be treated as an estimate, not a regulatory value.

UK CBAM operates on a comparable design principle: Finance Act 2026 establishes the charge, with the specific rate to be set through secondary legislation currently in draft/consultation, tied to UK ETS or domestic carbon price mechanisms. The exact UK CBAM rate has not yet been finalised in secondary legislation; exporters should monitor HMRC's consultation outcomes rather than plan against an assumed figure.

For a UK exporter, the practical point is this: you do not pay this cost directly. Your EU customer does. But a customer facing a variable, emissions-linked cost has every incentive to demand accurate data so they aren't over-declaring, and to prefer suppliers whose emissions profile is lower and better evidenced, because that directly reduces their certificate spend.

Commercial Risks for UK Exporters

Risk | Mechanism |

Loss of preferred supplier status | Customer shifts sourcing to a supplier with lower, better-evidenced emissions |

Procurement exclusion | Buyer's internal policy excludes suppliers who cannot provide verifiable data |

Contract renegotiation | Customer seeks to reallocate CBAM cost risk contractually |

Delayed shipments | Customs or customer holds on goods pending emissions evidence |

Customer switching | Buyer moves to an EU-based or lower-emissions alternative supplier |

Reputational impact | Customer flags data gaps internally, affecting future procurement rounds |

Supply chain disruption | Downstream delays where evidence packs are incomplete at the point of shipment |

None of these risks require a UK exporter to owe the EU a single euro directly. They are all downstream of the customer's own certificate exposure — which is why they are frequently underestimated by UK compliance teams focused only on their own legal position.

Contractual and Pricing Considerations

Carbon-cost allocation: Contracts need explicit clauses on who bears the commercial consequence of a CBAM-related cost increase — this is a negotiation point, not a settled default.

Incoterms implications: Delivery terms affect who is positioned as the technical importer of record, and therefore who carries the certificate obligation.

Warranties and emissions representations: Customers may seek contractual warranties on the accuracy of supplied emissions data — exporters should understand the liability this creates before agreeing.

Liability clauses: Where emissions data proves inaccurate, contracts should specify remedy, not leave it to dispute.

Pricing negotiations: Lower, well-evidenced emissions are becoming a genuine commercial differentiator, not just a compliance nicety.

Evidence obligations: Contracts should specify what evidence standard is required (e.g. third-party verification vs self-declared), since this materially affects the exporter's operational burden.

Penalties: Penalties: TAXUD and HMRC materials confirm that administrative penalties apply for false reporting or non-registration under both regimes. Specific penalty rates are set out in implementing and national instruments rather than in the primary legislation itself; exporters should verify current rates directly against the EU implementing texts and HMRC's secondary legislation as they are published.

Section 6: Sector-Specific Impact Analysis

The EU CBAM currently covers iron and steel, aluminium, cement, fertilisers, hydrogen and electricity, with future scope expansion under consideration. Exposure and documentation burden differ meaningfully by sector.

Iron & Steel

Steel is the UK's largest CBAM-affected export sector by exposure. UK Steel and associated sector briefings have reported order delays and increased requests for verified emissions data from EU buyers. Embedded emissions calculation is particularly complex in steel due to variation in production route (primary vs secondary/scrap-based production), which materially affects the emissions figure a supplier must defend.

Frameworks: Steel Export Readiness Scorecard; Typical EU Buyer Information Request template.

Friction point: Steel producers using mixed production routes across a single site face the hardest emissions-allocation problem in the entire CBAM scope — customers want route-specific, not site-average, figures.

Aluminium

Aluminium's principal complexity is production-route emissions calculation, not the direct/indirect distinction some suppliers assume applies. Under Annex II of the EU CBAM framework, aluminium is scoped to direct emissions only — indirect emissions from purchased electricity are not currently within the reporting boundary for this sector, unlike the treatment applied elsewhere in the regulation. Exporters should calculate and evidence direct process emissions precisely, without over-engineering electricity-sourcing disclosures the current scope does not require. Smelter-specific reporting adds further complexity where a single exporter sources from multiple upstream smelters, since each smelter's direct emissions profile must be tracked and evidenced separately.

Friction point: Aluminium exporters sourcing input metal from multiple smelters face a supply-chain data aggregation problem that steel producers with single-site production do not.

Cement & Clinker

Cement's exposure centres on process emissions (as distinct from combustion emissions) and installation-level reporting requirements. EU sector guidance addresses verification requirements for cement producers.

Friction point: Verification cost falls disproportionately on smaller cement producers, who often lack in-house capability to generate the process-emissions detail EU buyers now expect.

Fertilisers & Hydrogen

Fertiliser and hydrogen exporters face emissions methodology questions tied to production route — high-carbon production pathways face materially greater customer due-diligence scrutiny than low-carbon routes, directly affecting market competitiveness independent of price.

Friction point: Customer due diligence in these sectors functions as a de facto market filter — a supplier on a high-carbon production route may be commercially excluded even where its product is otherwise price-competitive.

Preparing for Future Scope Expansion

CBAM's current scope may extend to downstream products and broader value chains. EU Commission and Parliamentary commentary reference this as a general possibility, without confirmed dates or a defined product list. Manufacturers should treat scope expansion as a planning consideration, not a scheduled certainty.

Table — Sector Exposure Comparison

Sector | Primary Complexity | Documentation Burden |

Iron & Steel | Production-route emissions variation | High |

Aluminium | Direct-emissions-only scope (Annex II); multi-smelter sourcing complexity | High |

Cement | Process emissions; verification cost for SMEs | Medium–High |

Fertilisers & Hydrogen | Production-route customer scrutiny | Medium |

Section 7: Practical Action Framework

The 90-Day Executive Action Plan

Phase | Actions |

Week 1–2 | Identify all EU customers receiving CBAM-in-scope goods; assign a single internal CBAM data owner; audit existing emissions data against the Required Documentation Checklist (Section 3) |

First Month | Build the standing evidence pack per installation; establish the Customer Request Workflow (Section 3) with defined SLAs; brief Export Sales on first-response protocol |

First Quarter | Run a mock customer data request internally to test response time and consistency; review contract templates for CBAM-related clauses; confirm UK CBAM registration timeline relevance to the business |

Ongoing Governance | Quarterly review of evidence pack accuracy; monitor EU and UK regulatory updates via GOV.UK and TAXUD; maintain version-controlled emissions records per customer submission |

Building an Internal CBAM Programme

Ownership should not default informally to whoever answered the first customer email. Establish clear governance across Senior Management (accountability), Production and Operations (data), Finance (exposure modelling), Sustainability (methodology), and Sales/Export Teams (customer interface) — as detailed in the RACI matrix in Section 3.

Preparing Customer Evidence Packs

The evidence pack should be organised so any authorised team member can respond to a request without recreating work from scratch: emissions calculations, verification records, production documentation, supporting evidence, document control versioning, and a full audit trail. A well-organised, registry-compatible evidence pack functions as a direct commercial asset, not just an internal file.

Customer Communication Strategy

Respond to questionnaires with the standing evidence pack, not ad hoc calculations — consistency across customers is a credibility signal.

In procurement conversations, be prepared to explain your emissions methodology in plain terms, not just hand over a spreadsheet.

When a customer challenges a figure, route the technical explanation through whoever owns the methodology (Sustainability/Production), not through Sales.

Executive Readiness Checklist

Single named CBAM data owner identified

Evidence pack built and current for every EU-facing installation

Customer Request Workflow documented and tested

Contract templates reviewed for CBAM clauses

UK CBAM registration timeline tracked against business exposure

Governance RACI assigned and communicated internally

Section 8: Strategic Outlook (2026–2027)

Regulatory Developments to Watch

UK CBAM implementation from 1 January 2027 is the most concrete near-term development. Potential UK-EU ETS linkage, simplification proposals, and downstream product expansion are referenced in general policy commentary, without confirmed implementation dates. Monitor GOV.UK and TAXUD updates directly rather than treating these as scheduled certainties.

Competitive Implications

Carbon transparency is becoming a procurement differentiator independently of price. Exporters who can produce fast, consistent, well-evidenced emissions data are positioned to retain preferred-supplier status through 2026–2027; those who cannot are exposed to switching risk regardless of product quality or price competitiveness.

Board-Level Strategic Priorities

Treat CBAM readiness as a customer-retention investment, not a compliance cost centre.

Build governance now — retrofitting ownership under a live customer deadline is measurably slower and more error-prone.

Track UK CBAM registration timing in parallel with EU customer management, given the overlapping 2026–2027 window.

Engage with customer emissions expectations directly rather than waiting for a formal request to arrive.

Revisit contract templates before renewal cycles, not during a live dispute — this is the single highest-leverage action available to a UK exporter in the next 12 months.

Section 9: FAQ:

What information does my EU customer need from me under EU CBAM?

Embedded emissions data at product and installation level, production process documentation, verification evidence, and supporting records such as energy source mix. The exact scope varies by customer and sector, but the standing evidence pack described in Section 3 covers the common core.

Do I have legal obligations under EU CBAM if I'm only exporting from the UK?

No. The legal obligation to purchase and surrender CBAM certificates sits with the authorised EU importer, not the UK exporter. Your obligation to supply data is commercial, arising from customer relationships and contracts, not from EU CBAM statute directly.

What documents should I prepare before an EU customer requests emissions data?

Installation-level embedded emissions calculations, verification or third-party evidence, production process documentation, energy source data, and records of prior customer submissions for consistency. See the Required Documentation Checklist in Section 3.

Who should own CBAM compliance inside my business?

A single named owner, supported by the RACI structure in Section 3: Senior Management for accountability, Production/Operations for data, Sustainability for methodology, Finance for exposure modelling, and Export Sales for customer communication.

How should I respond if an EU customer rejects my emissions calculations?

Route the technical challenge to whoever owns your emissions methodology, not to Sales. Cross-check the disputed figure against your version-controlled evidence pack and previous submissions before responding — inconsistency across customers is the most common root cause.

How do EU CBAM, UK ETS and the UK's CBAM interact for British manufacturers?

EU CBAM (live from 1 January 2026) governs your EU customers' certificate obligations. UK CBAM (live from 1 January 2027, per Finance Act 2026) will separately apply if you import CBAM-in-scope goods into the UK. The two regimes run on different timelines and different legal bases — track both independently.

Section 10: References & Sources:

Key Authoritative Sources

European Commission, Directorate-General for Taxation and Customs Union (DG TAXUD) – Carbon Border Adjustment Mechanism. Published 18 March 2026. This is the European Commission's primary guidance portal covering the EU CBAM definitive regime, implementation guidance, authorised declarants, the CBAM Registry, emissions reporting requirements and related legislation.

GOV.UK (Department for Business and Trade) – Summary of European Commission Guidance on the EU CBAM for UK Exporters. Originally published 17 January 2024, last updated 4 December 2025. This guidance helps UK exporters understand how EU CBAM affects exports to the European Union and signposts relevant European Commission resources for compliance preparation.

HM Revenue & Customs (HMRC) / GOV.UK – Draft Regulations: Carbon Border Adjustment Mechanism (CBAM) – Emissions and Verification (Consultation). Published 8 April 2026. The consultation outlines the proposed UK CBAM emissions calculation methodology, verification requirements and administrative framework ahead of the UK's planned CBAM implementation in 2027.

GOV.UK – Carbon Border Adjustment Mechanism (CBAM): Policy Summary. Published 9 February 2026. This policy summary explains the objectives, scope, operation and legislative framework of the UK's Carbon Border Adjustment Mechanism, including the sectors covered and the government's implementation approach.

UK Parliament – House of Commons Library – Carbon Border Adjustment Mechanism (Research Briefing CBP-9935). Published 9 April 2026. This parliamentary research briefing provides an independent overview of both the EU and UK CBAM regimes, their policy rationale, implementation timelines, international trade implications and key considerations for UK businesses and policymakers.

Legal Disclaimer:

This report is published by Sekason Research Limited (Company No. 14339910), trading as CBAM Journal, and is provided for general informational purposes only. It does not constitute legal, financial, tax, or regulatory advice, and should not be relied upon as a substitute for advice from a qualified professional. No solicitor-client, advisor-client, or equivalent professional relationship is created by the purchase or use of this report.

While every effort has been made to ensure the information in this report is accurate and current as of its publication date, UK CBAM and EU CBAM regulations are subject to ongoing legislative and regulatory change. Sekason Research Limited makes no warranty, express or implied, as to the completeness, accuracy, or continued validity of the information contained herein, and accepts no liability for any loss or damage arising from reliance on this content.

Readers should independently verify all compliance obligations, deadlines, and financial exposures directly with HMRC, the European Commission, or a qualified legal or tax advisor before taking action. This disclaimer is governed by the laws of England and Wales. Read full disclaimer: https://www.cbamjournal.com/disclaimer

Comments