UK CBAM Cement Compliance Guide: What Importers Must Do Before 1 January 2027

- Ahtesham Shaikh

- 4 days ago

- 29 min read

CBAM Journal Regulatory Intelligence Report Compliance Obligations, Embedded Carbon Reporting, Financial Exposure and Implementation Roadmap for UK Cement Importers (2026–2027) Prepared by Sekason Research Limited, London

Section 1 — Executive Summary

The UK Carbon Border Adjustment Mechanism (UK CBAM) commences on 1 January 2027 and places a carbon charge on the emissions embodied in imported cement, alongside aluminium, fertiliser, hydrogen and iron and steel. Any business importing £50,000 or more of CBAM goods over a rolling 12-month period must register with HMRC, with the value of the CBAM good counting towards that threshold in all cases.

The single largest operational risk for cement importers is emissions data: the charge will be calculated using independently verified actual emissions data, verified by accredited ISO professionals, with government-published default emissions values available only as a fallback where actual data is unavailable.

The legislative framework is partially settled and partially in draft. Primary legislation proceeds through the Finance Bill 2025–26, confirmed by the government on 30 October 2024. HMRC published draft secondary legislation and opened a technical consultation on 10 February 2026, which closed on 24 March 2026.

The draft regulations cover tax returns and required content, record keeping, the weight of CBAM goods, and reimbursement arrangements. Critically, HMRC has not yet published UK penalty levels, the carbon price per tonne, or cement default emission factors. Only the £50,000 registration threshold and the sector scope are confirmed at numeric level.

The compliance clock is short. Registration is expected to open in late 2026. The first accounting period covers full-year 2027, reported through an annual tax return, before accounting periods become quarterly from 2028.

Cement importers that have not begun supplier engagement, commodity scope assessment and data-system preparation by mid-2026 face a compressed implementation window in which overseas verification lead times become the binding constraint.

This report converts the confirmed framework into an operational programme:

scope determination,

supplier emissions data strategy,

liability estimation,

record keeping,

governance

and a twelve-month implementation roadmap.

Executive Compliance Snapshot

Item | Position | Status |

Commencement | 1 January 2027 | Confirmed (HMRC policy summary) |

Registration threshold | £50,000 CBAM goods, rolling 12 months | Confirmed |

Sectors | Aluminium, cement, fertiliser, hydrogen, iron and steel | Confirmed |

Emissions data | Independently verified actual emissions; default values as fallback | Confirmed in principle; values unpublished |

Charge mechanism | Carbon price on embodied emissions, linked to UK ETS | Confirmed in principle; rate unpublished |

First reporting | Annual return for 2027 accounting period | Confirmed |

From 2028 | Accounting periods become quarterly | Confirmed (draft regulations) |

Penalties | Not yet specified in published guidance | Unpublished |

UK default emission factors (cement) | Not yet published | Unpublished |

Section 2 — Regulatory Context

Why the UK Introduced CBAM

UK CBAM places a carbon price on the emissions embodied in imports of specified goods. A plausible policy rationale — preventing the UK's domestic carbon pricing under the UK ETS from being undercut by imports produced in lower-carbon-cost jurisdictions — is not itself stated in HMRC's published material, which confirms the mechanism rather than its underlying purpose.

The government confirmed on 30 October 2024 that the mechanism would be introduced on 1 January 2027, with primary legislation carried through the Finance Bill 2025–26.

HMRC's policy summary states the mechanism plainly: CBAM "will place a carbon price on the emissions embodied in imports of specified goods" across the five named sectors, cement included.

For cement importers, the enforcement logic follows from that design. The charge attaches to embodied emissions, so the regulator's attention will fall on the quality of emissions data, the accuracy of import quantities and weights, and the completeness of records — the three elements the draft secondary legislation explicitly addresses. Compliance teams should treat data integrity, not tariff classification alone, as the primary audit surface.

Legislative Framework

The framework operates on two levels, and the distinction between them determines what is legally settled today. The Finance Bill 2025–26 provides the primary legislation establishing the charge. Beneath it, HMRC published draft secondary legislation on 10 February 2026 and consulted on the draft regulations and notices until 24 March 2026. The draft regulations set out the administrative machinery: tax returns and their required content, record-keeping obligations, the weight of CBAM goods, reimbursement arrangements, and the move to quarterly accounting periods from 2028.

The precise statutory instrument name and article numbering are not yet finalised in published form. Every administrative requirement described in this report that derives from the draft regulations is therefore consultation-stage material, subject to confirmation in the final statutory instrument. What is settled: the 1 January 2027 commencement, the five-sector scope, the £50,000 rolling threshold, the verified-actual-emissions-first data hierarchy, and the UK ETS-linked charge design.

What is not settled: penalty levels, the numeric charge rate, default emission values, and final administrative detail.

The practical consequence for a Compliance Manager is a two-track posture. Build systems now against the confirmed framework and the draft regulations as published, and maintain a monitoring process — assigned to a named individual — for the final statutory instrument, HMRC guidance, and the default values expected before commencement.

Cement Within UK CBAM Scope

Cement is explicitly listed among the five UK CBAM sectors in HMRC's policy summary, and HMRC's April 2026 communications pack for trade associations names cement as a sector for which trade bodies must cascade CBAM information to members and supply chains. Sector inclusion is therefore beyond doubt.

Product-level scope is not yet equally settled. HMRC has not published a UK commodity-code list for cement; this is an acknowledged limitation of currently available guidance. The EU regime provides the closest available reference for the product families likely to require assessment. Under Regulation (EU) 2023/956, Annex I, EU CBAM covers clinker (CN 2523 10), Portland cement (CN 2523 21/29), aluminous cement (CN 2523 30), other hydraulic cements (CN 2523 90) and certain cement-based articles (CN 6810–6812).

UK importers should map their import records against these product families now, and re-run the mapping against the UK list when HMRC publishes it.

Products Covered — Reference Scope Matrix

Product | Commodity Code (EU reference) | Included (EU) | UK Position |

Cement clinker | CN 2523 10 | Yes | UK list unpublished — assess |

Portland cement | CN 2523 21 / 2523 29 | Yes | UK list unpublished — assess |

Aluminous cement | CN 2523 30 | Yes | UK list unpublished — assess |

Other hydraulic cements | CN 2523 90 | Yes | UK list unpublished — assess |

Certain cement-based articles | CN 6810–6812 | Yes | UK list unpublished — assess |

EU codes shown as reference only; the UK product list will be confirmed in secondary legislation and HMRC guidance.

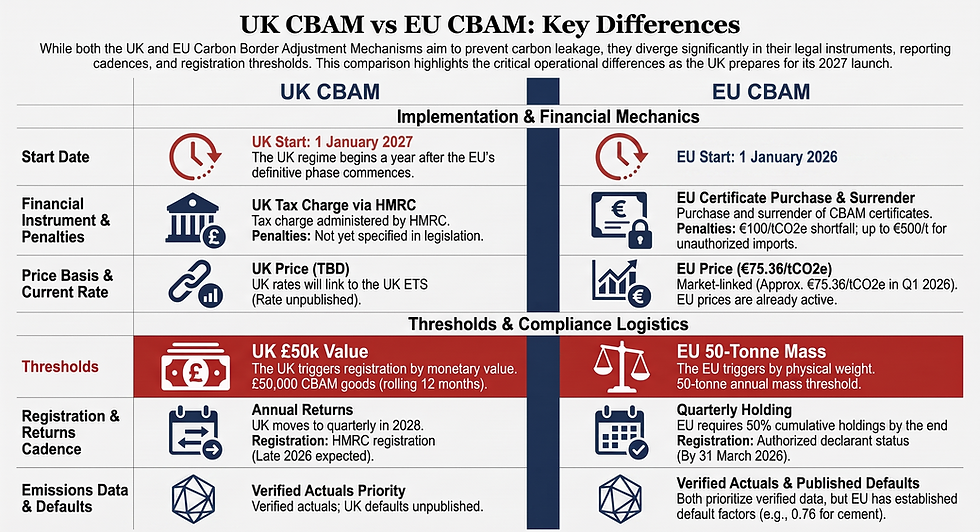

UK CBAM Compared with EU CBAM

The two regimes share a purpose and diverge in mechanics. The EU regime entered its definitive phase on 1 January 2026, with live certificate purchase and surrender obligations under Regulation (EU) 2023/956, as amended by Regulation (EU) 2025/2083. The UK regime commences a year later, on 1 January 2027, as a tax administered by HMRC — with no transitional reporting phase described in official sources. Importers operating across both jurisdictions cannot reuse an EU compliance model unchanged.

Dimension | UK CBAM | EU CBAM |

Start of obligations | 1 January 2027 | Definitive regime from 1 January 2026 |

Instrument | Tax charge administered by HMRC | Certificate purchase and surrender |

Threshold | £50,000 CBAM goods, rolling 12 months | 50-tonne annual mass threshold (Regulation (EU) 2025/2083, in force 20 October 2025, replacing the repealed €150 de minimis) |

Registration / authorisation | HMRC registration, expected to open late 2026 | Authorised CBAM declarant status; applications by 31 March 2026 allowed provisional importing pending decision |

Reporting cadence | Annual return for 2027; quarterly from 2028 | Annual declaration by 30 September of the following year; quarterly holding of 50% of cumulative embedded emissions |

Emissions data | Independently verified actual emissions; UK default values as fallback (unpublished) | Verified actual emissions or published default values (e.g. ~0.76 tCO₂e/t grey Portland cement) |

Price mechanism | Linked to UK ETS; rate unpublished | Certificate price approx. €75.36/tCO₂e in Q1 2026 |

Penalties | Not yet specified | €100/tCO₂e shortfall (inflation-indexed); €300–€500/t for importing without authorisation |

Section 3 — Compliance Obligations

Who Must Register

Registration is triggered by value: a business importing £50,000 or more of CBAM goods over a rolling 12-month period must register with HMRC. HMRC's policy summary is explicit that

"in all cases, the value of the CBAM good which the CBAM charge is based on, will count towards the £50,000 minimum registration threshold."

Registration is expected to open in late 2026, ahead of the 1 January 2027 commencement.

Two features of the threshold demand operational attention.

First, it is rolling, not calendar-based: threshold monitoring must be continuous, recalculated with each import, not checked annually.

Second, at £50,000 the threshold is low relative to commercial cement volumes — a small number of consignments will carry most importers past it.

The practical default for any regular cement importer is to assume registration will be required and to plan accordingly, while operating a documented monthly threshold-monitoring control for marginal cases.

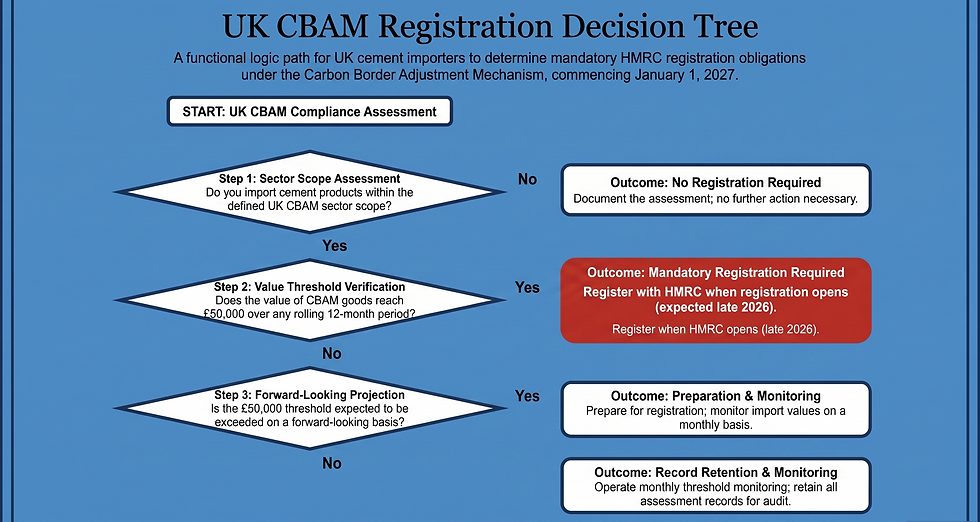

Registration Decision Tree

Question | If Yes | If No |

1. Do you import cement products in the UK CBAM sector scope? | Go to 2 | No registration; document the assessment |

2. Does the value of your CBAM goods reach £50,000 over any rolling 12-month period? | Register with HMRC when registration opens (late 2026 expected) | Go to 3 |

3. Is the threshold expected to be exceeded on a forward view? | Prepare registration; monitor monthly | Operate monthly threshold monitoring; retain records |

The mechanics of the forward-looking expectation test are not set out in currently published guidance; the sequence above reflects the consultation-stage framework and should be confirmed against the final statutory instrument.

Identifying In-Scope Cement Imports

Scope identification is a records exercise, and it should be run against the last 12 months of customs data before any supplier is contacted.

The workflow has four stages.

First, extract all import declarations for cement and cement-based products from customs records, including declared commodity codes, weights and values.

Second, map each declared code against the reference product families set out in Section 2 — clinker, Portland cement, aluminous cement, other hydraulic cements and cement-based articles — noting that the UK product list remains to be confirmed.

Third, attach each product line to its manufacturing supplier and production plant, not merely the invoicing intermediary, because emissions data must ultimately describe the plant that produced the goods.

Fourth, compute rolling 12-month CBAM goods value against the £50,000 threshold.

The output of this exercise is the scope register: a single controlled document listing every in-scope product, its commodity code, supplier, plant, annual volume and value.

Every later obligation — data collection, liability estimation, record keeping — keys off this register, which is why it is built first.

Borderline classifications are a live risk. Cement-based articles sit at the edge of the EU scope (CN 6810–6812), and the UK boundary is unpublished. Any product whose classification is uncertain should be flagged in the scope register and resolved with customs advisers before 2027, not after the first return.

Collecting Embedded Emissions Data

The UK charge will be calculated from independently verified actual emissions data, verified by accredited ISO professionals; the government will also publish default emissions values for use when actual data is unavailable.

That hierarchy makes supplier engagement the critical path of the entire compliance programme. Verified actual data cannot be generated by the importer — it must come from the overseas manufacturer's installation, and it must survive accredited verification.

The friction is considerable and should be planned for, not hoped away. Overseas cement producers may have no monitoring systems aligned to UK requirements, no experience of accredited verification, and no contractual obligation to supply the data. Verification capacity is a market constraint: verifiers must be engaged, scheduled and paid, and lead times should be planned for accordingly.

The EU experience is instructive — under EU CBAM, importers face a choice between verified actual emissions and default values, and CBAM Journal's analysis of 2 July 2026 found that default values increase certificate liability for most importers because of the mark-up embedded in defaults.

Whether UK default values will carry a comparable conservatism is unknown until HMRC publishes them; the prudent working assumption is that verified actual data will generally be financially preferable where the supplier's process is efficient.

Supplier Data Collection Workflow

Issue the supplier information request (Appendix D) to every supplier in the scope register, addressed to the production plant level.

Assess each response for data availability, methodology and verification status; record the assessment in the supplier readiness matrix (Section 6).

Where actual data exists, confirm the verification route with an accredited verifier and schedule verification ahead of the first accounting period.

Where actual data does not exist, record the default-value fallback for that supplier and quantify the expected cost consequence once UK defaults are published.

Embed data-delivery and verification obligations into supply contracts and purchase terms at the next renewal.

Re-run the assessment on a fixed cycle and before onboarding any new supplier.

Calculating UK CBAM Liability

The confirmed design is a carbon price applied to the embodied emissions of imported goods, linked to the UK ETS. HMRC has not published the charge rate, the calculation regulations in final form, or UK default emission factors.

The structural logic, however, is already clear enough to build an internal estimation model: liability is a function of import quantity, the emissions intensity of each product from each plant, and the applicable carbon price, adjusted for any relief available for carbon prices already paid abroad — a mechanism the draft framework anticipates in principle but has not yet published in operative detail, including its evidential requirements.

A finance team can replicate the following structure with its own volumes today, substituting HMRC's figures when published.

Worked Liability Example — illustrative; official HMRC values not yet published

Input | Value | Basis |

Imported product | Grey Portland cement | Scope register |

Annual import quantity | 10,000 tonnes | Importer's own records (illustrative volume) |

Emissions intensity | 0.76 tCO₂e/t | EU default factor for grey Portland cement — used purely as an illustrative proxy; UK factor unpublished |

Embodied emissions | 7,600 tCO₂e | Quantity × intensity |

Carbon price | €75.36/tCO₂e | EU CBAM certificate price, Q1 2026 — illustrative proxy; UK ETS-linked rate unpublished |

Indicative exposure | ≈ €573,000 | Before any relief for carbon prices already paid (mechanism not yet published) |

The example demonstrates the sensitivity that matters: at these illustrative values, each 0.1 tCO₂e/t of emissions intensity is worth roughly €75,000 a year on 10,000 tonnes. Supplier selection and data quality are therefore procurement decisions with a quantifiable carbon-cost dimension, not compliance formalities.

Record Keeping Requirements

The draft regulations explicitly include record keeping and the weight of CBAM goods among the legislative requirements, alongside tax returns and their required content.

Pending the final statutory instrument, importers should build the audit file to cover, at minimum: import declarations and customs records;

weights and quantities of CBAM goods per consignment;

emissions data and its methodology; verification records evidencing accredited verification;

supplier documentation supporting the emissions figures;

and evidence supporting any claim for relief on carbon prices already paid, for which the draft regulations' reimbursement arrangements are expected to set the evidential standard once published.

The statutory retention period for these records has not yet been specified in published guidance.

The operational standard to aim at is reconstructability: for any line of any return, the file must allow HMRC to trace from the declared charge back through the calculation, the emissions evidence and the verification record to the original import declaration. Building the file consignment-by-consignment from the first 2027 import is materially cheaper than reconstructing it before the first return.

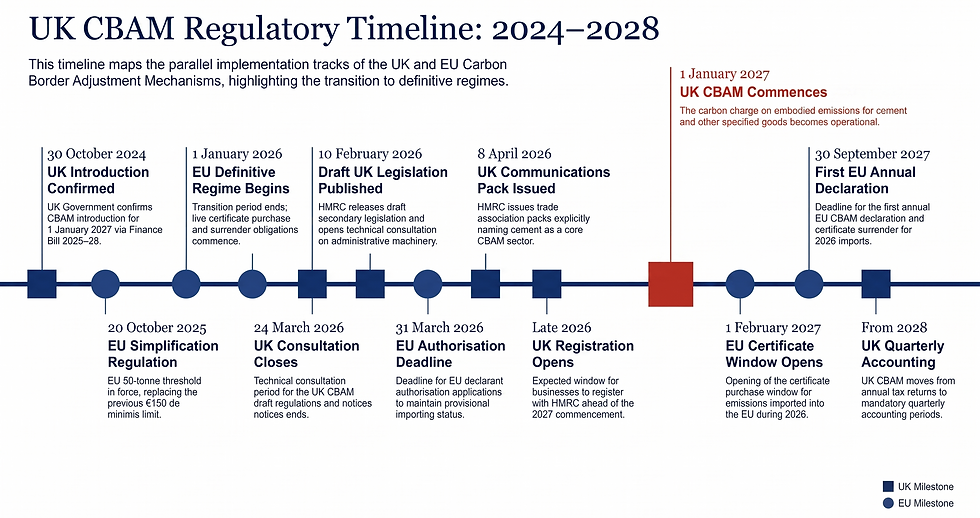

Section 4 — Key Dates and Compliance Timeline

Regulatory Timeline

Every confirmed date in the UK and EU regulatory chronology relevant to a cement importer is set out below. UK importers trading into both markets should read the two tracks together: the EU definitive regime is already live, and its deadlines fall due during the UK preparation window.

Complete UK CBAM Timeline (with EU reference points)

Date | Milestone | Regime |

1 October 2023 – 31 December 2025 | EU transitional phase: quarterly reporting only, no certificate surrender | EU |

30 October 2024 | Government confirms UK CBAM introduction on 1 January 2027; primary legislation via Finance Bill 2025–26 | UK |

20 October 2025 | Regulation (EU) 2025/2083 enters into force; 50-tonne mass threshold replaces €150 de minimis | EU |

1 January 2026 | EU definitive regime begins: certificate purchase and surrender obligations live | EU |

10 February 2026 | HMRC publishes draft secondary legislation; technical consultation opens | UK |

24 March 2026 | HMRC consultation closes | UK |

31 March 2026 | EU declarant authorisation applications deadline for provisional importing pending decision | EU |

End of each quarter, 2026 | EU quarterly holding requirement: 50% of cumulative embedded emissions | EU |

8 April 2026 | HMRC issues CBAM communications pack for trade associations, explicitly including cement | UK |

Late 2026 (expected) | UK CBAM registration expected to open | UK |

1 January 2027 | UK CBAM commences: carbon charge on cement and other specified goods operational | UK |

1 February 2027 | EU certificate purchase window opens for 2026 imports | EU |

30 September 2027 | First EU annual CBAM declaration and surrender deadline for 2026 imports | EU |

2027 | First UK accounting period; annual tax return and CBAM charge payment for 2027 imports | UK |

1 July each year | EU cancellation of unsurrendered prior-year certificates | EU |

From 2028 | UK accounting periods become quarterly | UK |

The exact filing and payment deadline for the first UK annual return has not yet been published; importers should treat the 2027 accounting period as the operative planning horizon and confirm the specific deadline once HMRC issues it.

Internal Preparation Timeline

The following roadmap is the analyst's recommended sequencing, working back from the 1 January 2027 commencement and the expected late 2026 registration opening. It is an operational recommendation, not a regulatory requirement.

12-Month Compliance Roadmap (July 2026 – June 2027)

July 2026 — Scope and governance. Build the scope register from 12 months of customs records; appoint the CBAM lead; convene the cross-functional team (Section 7, Step 4).

August 2026 — Supplier engagement. Issue the supplier information request (Appendix D) to all in-scope suppliers at plant level; open contract discussions on data obligations.

September 2026 — Data assessment. Score supplier responses in the readiness matrix; identify verified-data candidates and default-value fallbacks.

October 2026 — Verification and systems. Engage accredited verification for viable suppliers; specify record-keeping and data systems against the draft regulations.

November 2026 — Registration readiness. Prepare registration submissions for filing when HMRC opens the window; complete threshold documentation.

December 2026 — Dry run. Test the end-to-end process on Q4 import data: scope, weights, emissions, illustrative liability, audit file.

January 2027 — Go live. Commence consignment-level record capture from the first 2027 import; confirm registration status.

February–April 2027 — Operate and correct. Run monthly data-quality reviews; close gaps identified in live operation; monitor HMRC publications for default values and final guidance.

May–June 2027 — Assurance. Internal audit of the compliance file; management review; remediation ahead of the first annual return cycle.

Section 5 — Financial Exposure and Compliance Risk

How UK CBAM Creates Financial Exposure

Exposure under UK CBAM is driven by three variables: the volume of in-scope imports, the embodied emissions of those goods, and the carbon price applied — linked to the UK ETS — net of any relief for carbon costs already borne abroad, a mechanism anticipated but not yet named or detailed in published guidance. HMRC has published none of the numeric parameters: no charge rate, no penalty table, no default emission factors for cement.

The draft regulations reference reimbursement arrangements and administrative matters without numeric levels. Financial planning before publication is therefore scenario modelling by necessity, and every figure in this section that is not a confirmed EU parameter is labelled illustrative.

What is structurally certain is that emissions intensity is the controllable variable. Import volume is a commercial given and the carbon price is set by regulation, but the emissions attached to each tonne depend on which plant produced it and whether its actual performance can be verified. That is where compliance work converts directly into cost reduction.

Reporting accuracy carries its own financial dimension. Under the EU regime, the cost of getting it wrong is explicit — €100/tCO₂e of surrender shortfall, inflation-indexed, and €300–€500/t for importing without authorisation. UK penalty levels are unpublished, but the EU precedent indicates the order of severity that carbon border regimes attach to non-compliance, and UK importers should not plan on the assumption of leniency.

Estimating Future CBAM Costs

The scenario matrix below models annual exposure for a UK importer of 10,000 tonnes of grey Portland cement across three supplier emissions profiles. All values are illustrative — official UK values not yet published. Emissions intensities are drawn from the published EU default-factor ranges for cement (0.55–1.10 tCO₂e/t across cement types; ~0.76 tCO₂e/t grey Portland default; clinker 0.83–0.89 tCO₂e/t), and the carbon price proxy is the Q1 2026 EU certificate price of €75.36/tCO₂e.

Scenario Comparison Matrix — illustrative

Scenario | Emissions intensity (illustrative) | Embodied emissions (10,000 t) | Indicative annual exposure at €75.36/t |

Low-emission supplier (efficient modern kiln, verified actual data) | 0.55 tCO₂e/t | 5,500 tCO₂e | ≈ €414,000 |

Average supplier (at default level) | 0.76 tCO₂e/t | 7,600 tCO₂e | ≈ €573,000 |

High-emission supplier / default fallback | 1.10 tCO₂e/t | 11,000 tCO₂e | ≈ €829,000 |

The spread is the finding: on identical volume, the gap between the low and high scenarios is roughly €415,000 a year at the illustrative price. The EU guidance record supports the mechanism — importers face liability based on verified actual emissions or default values, and modern efficient kilns may reduce liability significantly. Procurement teams should run this matrix with their own volumes and treat the verified-data premium a good supplier can command as a price worth negotiating around.

Compliance Risks

The risk register below pairs each principal failure mode with its consequence and mitigation. It is designed to be lifted into the corporate risk system unchanged.

Risk | Consequence | Mitigation |

Missing supplier emissions data | Forced reliance on default values; under the EU regime, defaults increase liability for most importers, and UK defaults are unpublished | Early supplier engagement (Appendix D); contractual data obligations; default-cost quantification per supplier |

Incorrect commodity classification | In-scope goods omitted from returns, or out-of-scope goods charged; misstatement of the £50,000 threshold position | Scope register with customs-adviser sign-off on borderline codes; re-check against the UK list when published |

Poor documentation and weights records | Inability to evidence returns during HMRC audit; draft regulations explicitly require records of weights, emissions and import data | Consignment-level audit file from first 2027 import; reconstructability standard (Section 3) |

Registration failure | Operating outside the regime after exceeding the rolling £50,000 threshold | Monthly rolling-threshold monitoring control with named owner; registration prepared for the late-2026 window |

Inaccurate emissions reporting | Misstated charge; exposure to penalties whose UK levels are unpublished but whose EU analogues run to €100/tCO₂e and above | Accredited verification of actual data; internal review of every figure entering a return; management sign-off |

Verification capacity shortfall | Actual data unusable for want of accredited verification; forced default fallback | Verifier engagement scheduled in 2026, ahead of the first accounting period |

Section 6 — Sector-Specific Impact Analysis

Why Cement Is a High-Risk CBAM Sector

Cement carries structurally high embodied carbon because its emissions arise from the production process itself, not only from energy use. Under the EU regime — the fullest published treatment of cement's emissions profile — the covered emissions for cement are the direct process emissions from limestone calcination and kiln fuel combustion; indirect emissions from electricity are excluded for cement. Calcination releases CO₂ as a chemical consequence of converting limestone.

The published EU factors quantify the profile: ~0.76 tCO₂e per tonne of grey Portland cement, 0.83–0.89 tCO₂e/t for clinker, and 0.55–1.10 tCO₂e/t across other cement types.

That profile is why cement appears in both regimes' founding scope and why data quality dominates cement compliance economics. When most of the liability is process-driven, the difference between an efficient plant's verified figure and a conservative default value is the single largest lever an importer controls.

Whether UK CBAM will mirror the EU's direct-emissions-only treatment for cement is not yet stated: HMRC's published material confirms the verified-actual-emissions framework but contains no explicit statement on indirect emissions treatment for cement, and this remains an open question pending further guidance.

Which Cement Products Are Within Scope?

Section 2 established the position: cement's sector inclusion is confirmed for the UK, while the UK product-level commodity list is unpublished, leaving the EU's Annex I list as the working reference. The product families a UK importer should assess are clinker (CN 2523 10), Portland cement (CN 2523 21/29), aluminous cement (CN 2523 30), other hydraulic cements (CN 2523 90) and cement-based articles (CN 6810–6812).

The cement-based articles group deserves particular scrutiny in a construction supply chain, because it is the category where classification judgement — and therefore scope error — concentrates.

UK CBAM Cement Product Scope Matrix

Product | Commodity Code (EU reference) | Included (EU) | Comments |

Cement clinker | CN 2523 10 | Yes | Highest published emissions factors (0.83–0.89 tCO₂e/t) |

Portland cement (grey) | CN 2523 21 / 2523 29 | Yes | EU default ~0.76 tCO₂e/t |

Aluminous cement | CN 2523 30 | Yes | Verify classification against product chemistry |

Other hydraulic cements | CN 2523 90 | Yes | Wide factor range (0.55–1.10 tCO₂e/t) |

Cement-based articles | CN 6810–6812 | Yes (certain articles) | Principal borderline category; obtain classification advice |

UK product list to be confirmed in secondary legislation.

Embedded Carbon in Cement

Embedded carbon is the liability variable of the entire regime: CBAM Journal's technical analysis of 30 June 2026 confirms embedded carbon as the key liability determinant for UK CBAM from 1 January 2027.

For cement, the emissions to be captured divide into process emissions from calcination and combustion emissions from kiln fuel, per the EU methodology reference. The UK data hierarchy is confirmed at framework level: independently verified actual emissions first, verified by accredited ISO professionals, with published default values as the fallback.

The commercial implication of the fallback is documented on the EU side. CBAM Journal's 2 July 2026 analysis found that default values increase certificate liability for most importers because of the mark-up embedded in defaults.

An importer that cannot obtain verified data does not merely lose precision — it very likely pays for the shortfall. Until HMRC publishes UK default values, the size of that premium in the UK regime is unquantifiable, which is itself a planning fact: the value of securing verified supplier data cannot be precisely priced yet, but the direction is one-way.

Overseas Supplier Readiness

Supplier readiness is the least documented and most consequential variable in the programme. No region-by-region assessment of cement supplier readiness for UK CBAM is currently available in published guidance or market analysis; importers should treat this as an evidence gap to close through direct supplier engagement rather than regional assumption.

What the research record does support is the scale of trade response CBAM-class regulation produces. Analysis by the Global Trade Research Initiative found that Indian steel and aluminium exports to the EU fell 24.4% in FY2025 — from $7.71bn to $5.82bn, with steel down 35.1% to $3.05bn — attributed to CBAM reporting rules and anticipation of the full levy.

That evidence concerns steel and aluminium exporters rather than cement, but it establishes that carbon border regimes measurably affect trade flows in the sectors they cover; importers should treat counterparty continuity as a live consideration alongside data capability, without assuming the same scale of effect for cement.

Pending regional research, the readiness matrix below should be populated supplier-by-supplier from Appendix D responses rather than from regional generalisation.

Supplier Readiness Assessment Matrix (template)

Supplier | Country | Data Availability | Verification Status | Risk Rating | Action Required |

— | — | Actual / Partial / None | Accredited / In progress / None | High / Medium / Low | — |

Lessons from EU CBAM

The EU regime, in its definitive phase since 1 January 2026 after the October 2023 – December 2025 transitional period, provides the only operating precedent for UK preparation.

Five lessons transfer directly.

First, quarterly reporting during the transitional phase forced importers to build emissions data pipelines under deadline pressure — the UK regime offers no transitional phase in published sources, so UK importers must arrive at 1 January 2027 already operational.

Second, registration and authorisation are gating items: the EU set a 31 March 2026 application deadline to preserve provisional importing, and late applicants risked interruption; UK registration in late 2026 should be treated with the same priority.

Third, the default-versus-verified choice has a documented cost direction — defaults carry a liability premium for most importers.

Fourth, in-year obligations compound: the EU's quarterly 50% holding requirement turned an annual declaration into a continuous cash-flow and data exercise; the UK's move to quarterly accounting from 2028 will have a similar operational effect.

Fifth, deadlines cascade — certificate purchase from 1 February 2027, declaration and surrender by 30 September 2027, cancellation of unsurrendered certificates each 1 July — and organisations that mapped the full calendar early avoided forced positions.

EU Lessons Applicable to UK Cement Importers

EU experience | UK application |

Transitional quarterly reporting built data pipelines under pressure | No UK transitional phase described — be operational by 1 January 2027 |

Authorisation deadlines gated market access (31 March 2026) | Treat late-2026 UK registration as a gating milestone |

Default values carry a liability premium for most importers | Prioritise verified supplier data before UK defaults publish |

Quarterly 50% holding made compliance continuous | Prepare for UK quarterly accounting from 2028 now |

Deadline cascade (1 Feb / 30 Sep / 1 Jul) punished late planners | Map the full UK calendar into the corporate compliance diary |

Section 7 — Practical Action Framework

Step 1 — Determine Whether You Are Within Scope

Run the scope determination against records, not assumptions. Extract 12 months of import declarations; identify every cement product against the reference product families in Section 6; compute rolling CBAM goods value against the £50,000 threshold; and identify the legal entity that acts as importer and will carry the registration obligation.

The output is a documented in/out determination signed off by the compliance lead — retained even where the conclusion is "out of scope", because the rolling threshold means the determination must be re-performed monthly.

Step 2 — Map the Supply Chain

Emissions data lives at the production plant, so the map must reach past the invoice. For every in-scope product line, identify the manufacturing supplier, the specific production plant, any trading intermediaries, the customs broker handling declarations and the logistics providers holding weight records.

Where goods are bought through traders, establish now who will procure plant-level emissions data — the trader or the importer directly — because that single question determines whether verified data is obtainable at all. The output is a supply-chain map appended to the scope register.

Step 3 — Build an Embedded Carbon Data Strategy

Institutionalise data collection; do not run it as correspondence.

The strategy has five components:

a standard supplier questionnaire (Appendix D) issued at plant level;

a standard emissions data template so responses arrive comparable;

a stated verification requirement — independently verified actual emissions, verified by accredited ISO professionals — communicated to suppliers as the target standard;

an evidence-collection rule specifying the documents that must accompany every emissions figure;

and document control that versions every submission for the audit file.

Suppliers that cannot meet the standard are recorded as default-value fallbacks with a quantified cost consequence once UK defaults are published.

Embedded Carbon Data Collection Workflow: issue request → assess response → classify (verified-actual candidate / default fallback) → schedule verification → contract the obligation → re-assess on cycle.

Step 4 — Build Internal Governance

UK CBAM is a tax with procurement, customs, finance and data dimensions; no single function can own it alone.

Assign a named CBAM lead in Compliance;

give Procurement ownership of supplier data obligations and contract clauses;

Finance ownership of liability estimation and the eventual return;

Customs ownership of classification and the scope register;

Sustainability support on emissions methodology;

Legal review of contractual and regulatory positions; and Internal Audit a scheduled assurance review before the first return.

CBAM Responsibility Matrix (RACI)

Activity | Compliance | Procurement | Finance | Customs | Sustainability | Legal | Internal Audit |

Scope register and classification | A | C | I | R | I | C | I |

Supplier data collection | C | R | I | I | C | C | I |

Verification management | A | C | I | I | R | I | I |

Liability estimation | C | C | R | I | C | I | I |

Registration and returns | R/A | I | R | C | I | C | I |

Record keeping / audit file | A | C | C | R | I | I | R (review) |

Step 5 — Estimate Financial Exposure

Build the internal model from Section 5's structure: import volumes from the scope register, emissions intensities from supplier data where held and clearly labelled illustrative proxies where not, a carbon price assumption flagged as illustrative until HMRC publishes the UK ETS-linked rate, and a placeholder line for relief on carbon prices already paid, pending final rules.

Distinguish every illustrative input from every official one inside the model itself, so the model survives handover and audit. Refresh the model on each HMRC publication; the first refresh trigger is the release of UK default values.

Step 6 — Prepare for HMRC Reporting

Readiness is demonstrated by a dry run, not a policy document. Before 1 January 2027, confirm each item: documentation standards implemented at consignment level; systems capturing weights, quantities, values and emissions per import; the audit file structure live and tested; a defined reporting workflow from data capture to return sign-off; a quality-assurance step in which a second person checks every figure; and a management review that formally approves readiness.

UK CBAM Readiness Checklist — registration prepared for the late-2026 window; scope register complete and signed off; supplier data assessed and classified; verification engaged for actual-data suppliers; liability model operational; consignment-level record capture tested; RACI adopted; monitoring owner named for HMRC publications.

Step 7 — Twelve-Month Implementation Roadmap

Execute Section 4's roadmap as a managed project with monthly milestones: July 2026 scope and governance;

August supplier engagement;

September data assessment;

October verification and systems;

November registration readiness;

December dry run;

January 2027 go-live with consignment-level capture;

February–April operate, correct and monitor HMRC publications;

May–June internal audit and management review ahead of the first return cycle.

Report progress monthly to the governance team against these milestones; slippage in supplier engagement is the earliest predictor of a failed first return and should escalate immediately.

Section 8 — Strategic Outlook (2026–2027)

Expected Regulatory Developments

The published record identifies the specific developments to monitor. The final statutory instrument will follow the technical consultation that closed on 24 March 2026, converting the draft regulations — tax returns and content, record keeping, weights, reimbursement arrangements — into binding form. HMRC will publish default emissions values, which are confirmed as forthcoming but numerically unpublished; their release is the single most consequential pending publication for cement importers because it prices the fallback.

Registration will open, expected late 2026. HMRC's trade-association communications programme, running since 8 April 2026, indicates continuing guidance flow through the launch window. Assign each of these to the named monitoring owner established in Section 7.

Market Implications for Cement Importers

Carbon border regimes move trade flows before they collect revenue. The GTRI analysis of the EU regime recorded a 24.4% fall in Indian steel and aluminium exports to the EU in FY2025 — driven by reporting rules and anticipation of the levy, ahead of the definitive phase itself. GTRI also noted that CBAM arrives on top of existing safeguard quotas and anti-dumping duties, compounding the trade-policy load on affected supply chains.

For UK cement importers the strategic questions follow directly:

whether current suppliers will remain reliable counterparties under data and cost pressure;

whether sourcing should shift toward plants able to evidence lower verified emissions;

how carbon cost pass-through is handled in sales pricing; and which contractual protections — data obligations, price-adjustment clauses — go into the next procurement round.

These are decisions to take in 2026, while supplier alternatives remain open, not after the first liability crystallises.

Five Strategic Recommendations

Begin supplier engagement immediately — verified emissions data has the longest lead time of any compliance input.

Establish a cross-functional CBAM governance team with the RACI in Section 7 and a named accountable lead.

Prioritise verified actual emissions over default values wherever feasible; the EU record shows defaults carry a liability premium for most importers.

Build internal liability modelling capability now, with illustrative inputs clearly separated from official ones, and refresh on every HMRC publication.

Monitor HMRC continuously through a named owner, with the release of UK default values treated as an immediate re-planning trigger.

The single action that should leave this report today is the first one: issue the supplier information request (Appendix D) to every plant in the scope register this month, because every other item on this list — liability modelling, governance, registration readiness — depends on emissions data that only the supplier can provide, and that data has the longest lead time in the entire programme.

Section 9 — Frequently Asked Questions

Which cement products imported into the UK are subject to UK CBAM?

Cement is a confirmed UK CBAM sector from 1 January 2027, but HMRC has not yet published the UK product-level commodity code list. The EU regime's reference scope covers clinker (CN 2523 10), Portland cement (CN 2523 21/29), aluminous cement (CN 2523 30), other hydraulic cements (CN 2523 90) and certain cement-based articles (CN 6810–6812). Importers should assess against these families now and re-check when the UK list is published.

How do I know whether my business must register for UK CBAM?

Registration is required where the value of CBAM goods imported reaches £50,000 over a rolling 12-month period, with the value of the CBAM good counting toward the threshold in all cases. Registration is expected to open in late 2026, ahead of the 1 January 2027 commencement. Because the threshold is rolling, monitoring must be continuous rather than annual.

What information must I obtain from overseas cement manufacturers before importing?

Importers will need independently verified actual emissions data, verified by accredited ISO professionals, describing the emissions embodied in the goods at production-plant level. Where actual data is unavailable, government-published default emissions values may be used instead, but UK default values are not yet published. Supporting documentation on methodology and verification status should accompany every emissions figure for the audit file.

Should I use verified actual emissions or HMRC default emissions values?

Verified actual emissions are the primary basis under the UK framework, with defaults as the fallback where actual data is unavailable. The EU experience indicates that default values increase liability for most importers because of the conservatism embedded in defaults, and efficient plants can reduce liability significantly with verified data. Until HMRC publishes UK default values, verified actual data is the prudent target standard.

How can I estimate my company's UK CBAM liability before importing cement?

Model liability as import quantity × emissions intensity × carbon price, less any relief available for carbon prices already paid, labelling all inputs illustrative until HMRC publishes the UK ETS-linked rate and UK default values. EU reference factors (grey Portland ~0.76 tCO₂e/t; range 0.55–1.10 tCO₂e/t) and the Q1 2026 EU certificate price (€75.36/tCO₂e) provide illustrative proxies. Refresh the model on every HMRC publication.

How should Compliance, Procurement, Finance and Customs teams divide responsibility for UK CBAM compliance?

Compliance holds overall accountability, registration and returns; Procurement owns supplier emissions data and contract obligations; Finance owns liability estimation and payment; Customs owns classification and the scope register. Sustainability, Legal and Internal Audit provide methodology support, contractual review and pre-return assurance respectively. A named CBAM lead and a documented RACI prevent the ownership gaps that produce reporting failures.

Section 10 — References and Sources

Primary Legislative and UK Government Sources

The legal core of this report rests on HMRC's published policy summary and the draft secondary legislation consultation, which together establish the commencement date, sector scope, registration threshold, emissions data hierarchy and administrative framework. The Finance Bill 2025–26 carries the primary legislation; the final statutory instrument remains pending following the consultation that closed on 24 March 2026. The April 2026 communications resources confirm cement's inclusion in HMRC's trade-association engagement programme.

European Commission and EU Sources

EU sources provide comparative context and the only published numeric parameters for cement carbon border compliance: Regulation (EU) 2023/956 and its Annexes define the EU product scope and emissions boundaries, Regulation (EU) 2025/2083 sets the current threshold and declaration framework, and Commission-linked guidance supplies the cement default factors and implementation detail used here as clearly labelled illustrative proxies.

Industry and Market Sources

Market and analytical sources — the GTRI trade analysis, cement-specific EU compliance guidance and CBAM Journal's technical publications — supply the trade-impact evidence, default-value economics and embedded carbon analysis that inform the strategic sections. They are used for market insight and implementation commentary, subordinate to the primary legislative sources in the evidence hierarchy.

Appendix A — UK CBAM Legislative Timeline

Date | Event |

30 October 2024 | Government confirms UK CBAM; commencement set at 1 January 2027; primary legislation via Finance Bill 2025–26 |

10 February 2026 | Draft secondary legislation published; HMRC technical consultation opens |

24 March 2026 | Consultation closes |

8 April 2026 | HMRC communications pack for trade associations issued (cement named) |

Late 2026 (expected) | Registration expected to open |

1 January 2027 | UK CBAM commences |

2027 | First (annual) accounting period |

From 2028 | Quarterly accounting periods |

Appendix B — Glossary

Embedded Carbon — the greenhouse gas emissions embodied in an imported good, the variable on which the UK CBAM charge is calculated.

Actual Emissions — plant-specific emissions data, which under UK CBAM must be independently verified by accredited ISO professionals.

Default Emissions Values — government-published fallback values usable where actual data is unavailable; UK values unpublished.

UK ETS — the UK Emissions Trading Scheme, to which the CBAM charge is linked.

CBAM Goods — goods in the specified sectors: aluminium, cement, fertiliser, hydrogen, iron and steel. Independent Verification — accredited third-party confirmation of actual emissions data.

Accounting Period — annual for 2027; quarterly from 2028.

Registration Threshold — £50,000 of CBAM goods over a rolling 12-month period.

Appendix C — Key HMRC Resources

Resource | Reference |

CBAM Policy Summary | gov.uk — Carbon Border Adjustment Mechanism (CBAM): Policy Summary (updated 9 February 2026) |

Draft regulations and technical consultation | gov.uk — Draft regulations: Carbon Border Adjustment Mechanism (10 February 2026) |

Communications resources for trade associations | gov.uk — CBAM communications resources (8 April 2026) |

Appendix D — Supplier Information Request Template

To be issued at production-plant level for each supplying plant.

Production facility: plant name, address, country, and the specific plant(s) producing goods supplied to us.

Products supplied: product descriptions and commodity codes for all cement products supplied.

Emissions data: do you hold plant-level embodied emissions data for these products? State the figure(s) in tCO₂e per tonne and the period covered.

Methodology: describe the monitoring and calculation methodology used to produce the emissions figures.

Verification status: have the emissions figures been independently verified? Provide the verifier's name, accreditation, and the verification statement.

Carbon price paid: state any carbon price paid in the country of production in respect of these emissions, with supporting evidence.

Supporting documentation: attach the documents evidencing items 3–6.

Contact: name the individual responsible for emissions data requests at the plant.

Appendix E — Compliance Manager's Readiness Checklist

☐ Scope register built from 12 months of customs records and signed off

☐ Rolling £50,000 threshold monitoring control operating with a named owner

☐ Supply chain mapped to production-plant level

☐ Supplier information requests (Appendix D) issued to all in-scope suppliers

☐ Supplier responses assessed; verified-actual candidates and default fallbacks classified

☐ Accredited verification engaged for actual-data suppliers

☐ Liability model built with illustrative inputs clearly separated from official ones

☐ Governance RACI adopted; CBAM lead named

☐ Consignment-level record capture and audit file tested in a dry run

☐ Registration prepared for the expected late 2026 window

☐ Named owner monitoring HMRC publications (final regulations, default values, guidance)

☐ Internal audit review scheduled before the first return

Sources Used in This Report

The following authoritative government publications, legislation, regulatory guidance, industry resources, and research publications were used in preparing this report:

HM Revenue & Customs — Draft regulations: Carbon Border Adjustment Mechanism (CBAM) (10 February 2026). Available at: https://www.gov.uk/government/consultations/draft-regulations-carbon-border-adjustment-mechanism-cbam

HM Revenue & Customs — Carbon Border Adjustment Mechanism (CBAM): Policy Summary (9 February 2026, updated). Available at: https://www.gov.uk/government/publications/carbon-border-adjustment-mechanism-cbam-policy-summary/carbon-border-adjustment-mecha

HM Revenue & Customs — CBAM Communications Resources for Trade Associations (8 April 2026). Available at: https://www.gov.uk/government/publications/carbon-border-adjustment-mechanism-cbam-communications-resources

European Commission — Regulation (EU) 2023/956 (CBAM Regulation) (10 May 2023). Available at: https://taxation-customs.ec.europa.eu

European Commission / DEHSt — Guidance Document on CBAM Implementation for Importers (21 November 2023). Available at: https://taxation-customs.ec.europa.eu/system/files/2023-11/CBAM%20Guidance_EU%20231121%20for%20web_0.pdf

European Commission / DEHSt — CBAM Definitive Regime from 2026 (18 March 2026). Available at: https://www.dehst.de/EN/Topics/CBAM/CBAM-definitive-regime-2026/cbam-definitive-regime-2026_node.html

cbam-compliance.io — CBAM for Cement & Clinker Imports (Current as of 2025–2026; undated). Available at: https://cbam-compliance.io/cement

Times of India / Global Trade Research Initiative (GTRI) — EU CBAM Challenge: GTRI Warns of Trade Hit, Urges India to Fast-Track… (19 September 2025). Available at: https://timesofindia.indiatimes.com/business/india-business/eu-cbam-challenge-gtri-warns-of-trade-hit-urges-india-to-fast-track-...

CBAM Journal — EU CBAM Definitive Regime 2026 (28 May 2026). Available at: https://www.cbamjournal.com/post/eu-cbam-definitive-regime-2026

CBAM Journal — EU CBAM Certificates Explained: How the Cost Is Calculated (22 June 2026). Available at: https://www.cbamjournal.com/post/eu-cbam-certificates-explained-how-the-cost-is-calculated

CBAM Journal — What Is Embedded Carbon Under UK CBAM? The Technical Definition Every Importer Must Understand (30 June 2026). Available at: https://www.cbamjournal.com/post/what-is-embedded-carbon-under-uk-cbam

CBAM Journal — UK CBAM Registration and Liability Thresholds: A Compliance Manager's Guide (8 June 2026). Available at: https://www.cbamjournal.com/post/uk-cbam-registration-hmrc-50000-threshold

CBAM Journal — UK CBAM Importer Compliance Readiness 2027 (24 May 2026). Available at: https://www.cbamjournal.com/post/uk-cbam-importer-compliance-readiness-2027

IACBAM — HMRC Publishes Official UK CBAM Policy Summary (2026). Available at: https://www.iacbam.org/updates/uk-cbam-official-policy-summary-2026

Legislation.gov.uk — The Greenhouse Gas Emissions Trading Scheme (Amendment) Order 2026 (30 November 2025). Available at: https://www.legislation.gov.uk/ukdsi/2026/9780348277067/note

Legal Disclaimer

This report is published by CBAM Journal, an independent regulatory intelligence publication operated by Sekason Research Limited (London, UK). It is provided for informational and educational purposes only and does not constitute legal, tax, customs, accounting, environmental, or professional advice. Although every effort has been made to ensure accuracy using official sources available at the time of publication, UK CBAM legislation, HMRC guidance, secondary regulations, administrative procedures, and emissions methodologies may change after publication.

Readers should verify all regulatory requirements against the latest official publications issued by HM Revenue & Customs (HMRC), the UK Government, and other relevant authorities before making business, compliance, or commercial decisions. Where future regulations, consultations, draft legislation, expected implementation measures, projections, or illustrative examples are discussed, they should not be interpreted as final legal requirements or guarantees of future regulatory outcomes.

Neither Sekason Research Limited nor CBAM Journal accepts any liability for any loss, damage, or consequences arising from reliance on this report. Organisations should seek independent professional advice appropriate to their specific circumstances before taking compliance or commercial action.

Full Legal Disclaimer: https://www.cbamjournal.com/disclaimer

Comments