EU CBAM Default Values vs Verified Emissions

- Ahtesham Shaikh

- 1 hour ago

- 19 min read

Strategic Compliance Guidance for Minimising CBAM Certificate Costs Under the EU Definitive Regime (2026–2027)

Prepared by CBAM Journal · Sekason Research Limited · London

SECTION 1 — Executive Summary

Commission default values increase CBAM certificate liability for most importers, because the mark-up built into them under Implementing Regulation (EU) 2025/2621 sits above best-available data as a matter of design. Verified, installation-specific emissions are financially preferable in most cases as a result, and are the methodology Regulation (EU) 2023/956 treats as standard.

The legal basis for both routes is set out in Article 7(2)(a) and Annex IV (defaults as fallback) and Article 8 and Annex VI (verification), with Commission Implementing Regulation (EU) 2025/2621 formalising defaults for the definitive regime that began on 1 January 2026.

That start date changed the nature of the obligation: certificates must now be purchased and surrendered against declared emissions, replacing the reporting-only duties of the transitional period. The single largest lever a Compliance Manager controls over the resulting liability is the choice between a Commission default and a verified, installation-specific figure — a choice that is not a standing election but is conditional on whether actual data is genuinely unavailable.

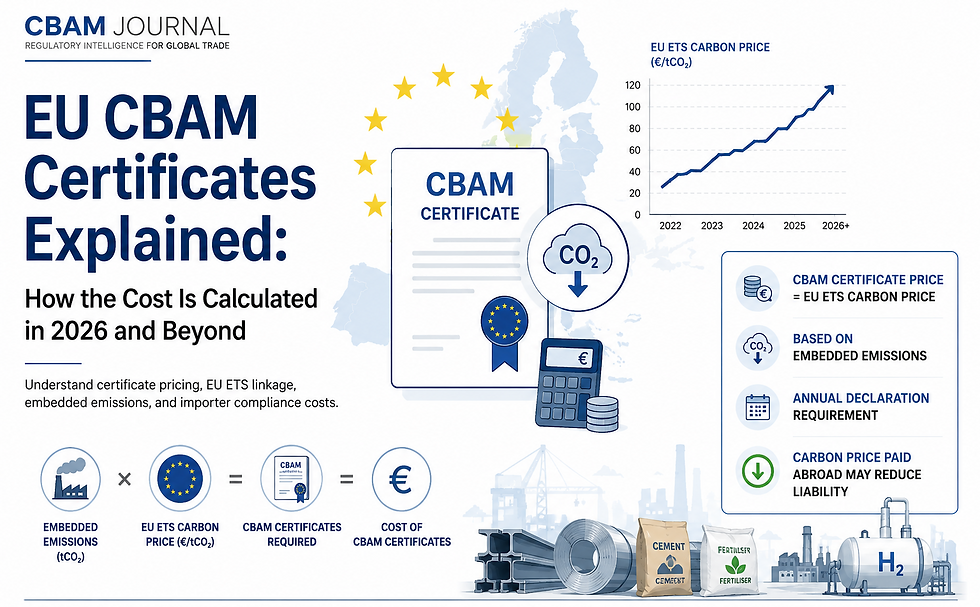

The certificate cost itself is calculated as embedded emissions minus free allocation, multiplied by the EU ETS carbon price, so any inflation in the emissions figure converts directly into euros owed. With the EU ETS spot price at €75.51/tCO₂ (CBAM Journal, June 2026), that sensitivity is material at import volume. Every importer defaulting by habit rather than by necessity is very likely overpaying for CBAM certificates.

This report sets out when default values may lawfully be used, what verification and declaration require in practice, how to build internal governance around the decision, and how to prioritise supplier engagement by sector so that compliance resource is spent where it reduces the most liability.

UK CBAM, launching 1 January 2027, follows the same conceptual logic — verified data preferred, defaults available but expected to be punitive for efficient producers — though its default-values framework remains in HMRC guidance rather than a consolidated implementing regulation at the time of writing.

Table 1 — Key Findings at a Glance

Issue | Business Impact | Recommended Action |

Default values carry a built-in mark-up over best-available data | Certificate obligations rise for efficient producers who default by habit | Request verified data before defaulting; treat defaults as an exception, not a routine |

EU definitive regime is live now; UK CBAM is not | EU certificate cost exposure is immediate; UK exposure is a 2027 planning problem | Sequence supplier engagement — EU first, UK preparation in parallel |

No published penalty or cost figures exist for defaulting itself | Financial exposure must be modelled from mechanism, not quoted from a rate card | Build internal cost-sensitivity models using the €75.51/tCO₂ ETS price and supplier-specific emissions ranges |

UK default values and verification rules remain in guidance form | UK compliance planning cannot yet rely on a finalised statutory instrument | Monitor HMRC publications through 2026; do not assume EU rules transpose directly |

Supplier data quality varies sharply by sector | Steel and aluminium carry the highest default-value cost risk | Prioritise supplier verification spend on steel and aluminium before cement, fertilisers, hydrogen and electricity |

SECTION 2 — Regulatory Context

Evolution of EU CBAM Default Values

Default values did not begin as a definitive-regime instrument. The Commission first published default values for the transitional period on 22 December 2023, when CBAM obligations were reporting-only and no certificate surrender applied.

That transitional framework — supported by Commission Implementing Regulation (EU) 2023/1773 — allowed importers to use Commission-supplied defaults where actual data was unavailable, with a cut-off of 31 July 2024 after which alternative methods, rather than the original transitional defaults, applied.

The definitive regime that began on 1 January 2026 changed the stakes entirely. Reporting became liability. Every tonne of embedded emissions declared, whether verified or defaulted, now converts into a certificate obligation priced against the EU ETS. Commission Implementing Regulation (EU) 2025/2621 re-established default values for this environment, and the Commission's policy intent — encouraging the collection of verified, installation-specific data rather than reliance on defaults — is expressed structurally through the mark-up built into those default figures rather than through a stated penalty.

Legal Basis

The obligation hierarchy an importer needs to hold in mind during any default-value decision:

Regulation (EU) 2023/956, Article 7(2)(a) and Annex IV — establishes that actual emissions data is required where available, and defines the circumstances in which default values may substitute for it.

Regulation (EU) 2023/956, Article 8 and Annex VI — sets the verification requirements for actual emissions data, including the requirement for an EU-accredited verifier.

Regulation (EU) 2023/956, Article 6 — governs the content of the CBAM declaration itself.

Regulation (EU) 2023/956, Article 14 — governs the CBAM Registry, the system of record for declarations.

Commission Implementing Regulation (EU) 2025/2621 — the operative default-values instrument for the definitive regime.

Article 7 and Annex IV tell the importer whether they may use a default. Article 8 and Annex VI tell them what is required if they do not. Article 6 and Article 14 tell them how the resulting figure — verified or defaulted — must be declared and where. 2025/2621 supplies the numbers.

Actual Emissions vs Default Values

Three tiers of emissions data exist under the definitive regime, and only one is the legally preferred methodology:

Actual emissions — installation-specific data supplied by the overseas producer, unverified.

Verified emissions — actual emissions data confirmed by an EU-accredited verifier under Article 8 and Annex VI. This is the methodology the Regulation treats as standard.

Default values — Commission-established figures under 2025/2621, available only where actual data cannot be obtained.

Table 3 — Actual Emissions vs Default Values

Criteria | Verified Actual Emissions | Commission Default Values |

Legal status under Article 7(2)(a) | Preferred methodology | Permitted fallback only |

Verification requirement | Mandatory (Article 8, Annex VI) | Not required — Commission-set figure |

Cost structure | Reflects true installation performance | Includes a mark-up over best-available data |

Supplier dependency | High — requires supplier cooperation and data access | None — usable without supplier engagement |

Typical outcome for efficient producers | Lower certificate obligation | Higher certificate obligation |

Why Default Values Include Mark-Ups

The mark-up built into Commission default values under 2025/2621 exists for one structural reason: it removes the financial incentive to default by convenience. If default values matched the average of actual emissions, importers would have no reason to bear the cost and effort of supplier verification — they would simply take the default every time. By setting defaults above best-available data, the Commission converts verification from a compliance nicety into a cost-reduction exercise.

The specific percentage mark-up by product and country is set out in the annexes to Implementing Regulation (EU) 2025/2621 and should be checked directly for any client-specific calculation.

Framework — Legal Hierarchy

EU Regulation (2023/956) → Implementing Regulations (2025/2621 and related acts) → Verification (Article 8/Annex VI) → Declaration (Article 6/Article 14) → Certificates (surrender against EU ETS price)

Table 2 — Comparison of Regulatory Instruments

Regulation | Purpose | Applies To | Importance |

Regulation (EU) 2023/956 | Core CBAM Regulation — establishes the mechanism, declaration and verification requirements | All EU CBAM importers | Foundational — every other instrument sits beneath this |

Commission Implementing Regulation (EU) 2023/1773 | Transitional-period rules, including original default values | Importers during the reporting-only phase (pre-2026) | Historical context; superseded for definitive-regime purposes |

Commission Implementing Regulation (EU) 2025/2621 | Definitive-regime default values, with mark-up methodology | Importers using default values under the definitive regime | Directly operative — governs every default-value declaration from 2026 |

SECTION 3 — Compliance Obligations

When May Default Values Be Used?

Article 7(2)(a) and Annex IV permit default values only where actual installation-specific data is not available to the importer. The Regulation does not treat this as a standing election — it is conditional on the absence of actual data, not a preference the importer can exercise freely once verified data becomes obtainable. Declarations relying on defaults must specify which default value was used and cite the implementing regulation reference under Article 6, meaning the choice is visible and auditable at the point of submission, not a background assumption.

Verification Requirements

Actual emissions data must be confirmed by a verifier accredited within the EU under the CBAM verification framework established by Article 8 and Annex VI. This applies whether the data originates from the importer's own analysis or is supplied by the overseas installation. Detailed documentary evidence standards and audit checklist items should be confirmed directly with the appointed verifier ahead of each declaration cycle.

Declaration Requirements

Article 6 sets the content requirements for the CBAM declaration: total embedded emissions, the resulting number of certificates, and — where a default is used — the specific default value applied together with its implementing regulation reference. Article 14 governs the CBAM Registry, the system through which the declaration is submitted and recorded.

A default-value declaration is therefore not anonymous within the system: it is tied to a named regulation and figure, which becomes the basis for any subsequent audit or Commission review.

Internal Governance Responsibilities

The Practical Action Framework in Section 7 depends on clear function ownership being assigned in advance:

Compliance — owns the legal interpretation of whether a default may be used and ensures the declaration cites the correct implementing regulation.

Procurement — owns the supplier relationship and is responsible for requesting verified emissions data as part of ongoing supplier engagement.

Sustainability — typically holds or coordinates the emissions data itself and liaises with accredited verifiers.

Finance — owns the certificate cost forecast and the budget impact of default-value versus verified-emissions declarations.

Internal Audit — reviews the evidence trail supporting each default-value decision, particularly where declarations will be scrutinised externally.

Table 4 — Compliance Obligation Matrix

Obligation | Regulation | Responsible Function | Frequency |

Determine whether actual data is available | Article 7(2)(a), Annex IV | Compliance, Procurement | Per consignment / per declaration cycle |

Verify actual emissions data | Article 8, Annex VI | Sustainability (coordinating accredited verifier) | Per supplier / per reporting period |

Apply correct default value where used | Implementing Regulation (EU) 2025/2621 | Compliance | Per declaration where defaults apply |

Submit CBAM declaration | Article 6 | Compliance | Annually (definitive regime) |

Maintain CBAM Registry record | Article 14 | Compliance | Ongoing |

Approve default-value use internally | Internal governance policy | Compliance, Finance, Procurement, Sustainability, Internal Audit | Per declaration where defaults apply |

Framework — Importer Compliance Workflow

Supplier → Data Collection → Verification → Decision (actual/verified vs default) → Declaration → Certificates

SECTION 4 — Key Dates and Deadlines

EU CBAM Timeline

Date | Event | Required Action |

1 October 2023 | Start of EU CBAM transitional period (reporting only) | Begin quarterly reporting; no certificate obligation yet |

22 December 2023 | Commission publishes default values for the transitional period | Available for use where actual data unobtainable during transition |

31 January 2024 | First CBAM quarterly report deadline (transitional period) | Submit first transitional quarterly report |

31 July 2024 | Cut-off for use of the original transitional-period default values | Transition to alternative methods where original transitional defaults no longer apply |

1 January 2026 | Start of EU CBAM definitive regime | Certificate purchase and surrender obligations become active; Implementing Regulation (EU) 2025/2621 default values apply |

31 May, annually | Deadline to surrender CBAM certificates for the previous reporting year | Complete certificate purchase and surrender for prior-year declared emissions |

Annual Compliance Calendar

The definitive regime converts the dates above into a recurring annual cycle rather than a one-off transition. Supplier engagement and verification work needs to be complete well ahead of the 31 May surrender deadline, since verification by an accredited party (Article 8, Annex VI) is not instantaneous and default-value declarations still require the correct implementing-regulation citation prepared in advance.

A detailed month-by-month operational calendar should be built directly against HMRC and Commission procedural guidance on submission windows once published; the confirmed anchor point remains 31 May.

Divergence: the EU definitive regime is fully operational now; UK CBAM does not launch until 1 January 2027, with HMRC continuing its "importer compliance readiness" workstream through 2026. Post-2027 UK reporting and payment deadlines are not yet fully detailed in published guidance.

SECTION 5 — Financial Exposure and Risk

Why Default Values Increase CBAM Costs

The certificate cost mechanism is straightforward: CBAM cost = (total embedded emissions − free allocation) × EU ETS carbon price. Because default values under 2025/2621 include a mark-up over best-available data, using a default rather than verified actual emissions increases the "total embedded emissions" term in that equation directly — and every additional tonne of embedded emissions is priced at the prevailing EU ETS rate, cited at €75.51/tCO₂ (CBAM Journal, June 2026).

The mechanism does not require a published penalty figure to be financially significant: the mark-up itself is the cost.

Cost Comparison Framework

Product- and country-specific default-value figures are not used here; the table below illustrates the calculation logic only, using clearly hypothetical inputs. It should not be read as a published default value and should not substitute for the actual figures in the annexes to Implementing Regulation (EU) 2025/2621.

Table 6 — Illustrative Cost Comparison (Hypothetical Inputs — Not Published Figures)

Scenario | Embedded Emissions (tCO₂, illustrative) | Certificates Required (illustrative) | Certificate Cost at €75.51/tCO₂ |

Verified actual emissions | Lower — reflects installation performance | Fewer | Lower total cost |

Commission default value applied | Higher — includes regulatory mark-up | More | Higher total cost |

Difference | Mark-up amount (see Implementing Regulation (EU) 2025/2621 annexes for the published figure) | Additional certificates required | Additional cost exposure, scaling with volume and mark-up size |

The cost differential scales with import volume: for a high-volume importer, even a modest mark-up compounds into a material annual figure once multiplied across every consignment defaulted rather than verified.

Risk Assessment Matrix

Table 7 — Risk Matrix

Risk | Likelihood | Impact | Mitigation |

Overpaying for certificates by defaulting where verified data was obtainable | High, for importers without an active supplier-engagement process | High — direct, recurring financial cost | Make verified-emissions requests the default first step, not the fallback |

Verification delays pushing declarations toward default use by necessity | Medium — dependent on supplier and verifier capacity | Medium to high, depending on volume | Start supplier verification requests well ahead of the 31 May surrender deadline |

Incorrect default-value citation in the declaration | Low to medium | Medium — audit and Registry accuracy risk | Assign Compliance as sole owner of default-value reference selection |

UK CBAM default-values framework changing before 2027 launch | Medium — UK rules remain in guidance form | Medium — planning assumptions may need revision | Track HMRC publications through 2026 rather than assuming EU parity |

Supplier unwillingness or inability to provide verified data | Medium to high, especially for less mature overseas suppliers | High for affected consignments | Prioritise supplier engagement by sector risk (see Section 6) |

Framework — Cost Decision Tree

Can verified emissions be obtained? → Yes: use verified emissions → No: apply default values → assess additional certificate cost → prioritise supplier engagement for future declarations

SECTION 6 — Sector-Specific Impact Analysis

Why Default Values Affect Each CBAM Sector Differently

The default-versus-actual mechanism applies uniformly across CBAM sectors, but its financial consequence does not. Sectors differ in production complexity, the extent of upstream emissions requiring verification, and how mature their typical overseas suppliers are at providing installation-specific data. This section orders sector priority by financial exposure so that compliance resource is not spread evenly across sectors that do not carry equal risk.

Steel

Steel is explicitly identified as a complex good under CBAM, meaning upstream emissions — from ironmaking through refining — must themselves be verified for inclusion in the declaration, not just the final processing step. Because the Commission default reflects a generic industry-wide profile rather than mill-specific performance, it is likely to sit above verified actuals for efficient producers, which is where the largest certificate-cost savings from verification arise. Steel importers therefore face the largest potential savings from verification, but also the largest documentation burden in achieving it.

Aluminium

For UK CBAM specifically, verified actual emissions will in most cases produce a lower liability than UK Government default values, making supplier engagement critical rather than optional for aluminium importers. EU CBAM similarly treats aluminium as a complex good requiring upstream verification wherever actual data is used; whether the same lower-liability finding holds under EU CBAM specifically has not yet been separately confirmed and should be checked before being relied on for EU-only declarations.

Cement

Cement is a core CBAM sector, and the general mark-up principle applies to it as it does elsewhere: default values are structured to penalise reliance on them relative to actual data. Cement-specific numerical default values and clinker-intensity figures are not yet published in a form suitable for a quantified comparison to steel and aluminium exposure; these should be sourced directly from the relevant annexes to Implementing Regulation (EU) 2025/2621 before a cement-focused update is issued.

What can be stated with confidence is the direction: verified production data reduces liability relative to conservative Commission defaults, and the incentive structure described in Section 2 applies to cement without qualification.

Fertilisers

Fertilisers are included in CBAM, and the same default-versus-actual rule applies, with default values inflated by the standard mark-up mechanism.

The commercial case for verification follows the same logic as other sectors: a default set above best-available data converts supplier engagement into a cost-reduction exercise rather than a compliance formality.

Hydrogen & Electricity

For electricity, default values are mandatory unless justified actual data is used, per the draft and consultation materials referenced — a stricter default-bias than applies elsewhere. Hydrogen is included in CBAM on the same actual-versus-default logic as other sectors: verified data must be used if available, with defaults applying otherwise.

The available guidance for these two sectors is comparatively less developed than for steel or aluminium, reflecting their draft/consultation status; specific grid emission factor figures and the finalised electricity verification framework should be confirmed directly once the Commission's implementing measures are finalised.

Table 8 — Sector Comparison Matrix

Sector | Complexity | Default Value Risk | Verification Priority | Financial Exposure |

Steel | High — complex good, upstream verification required | High | Highest | Highest — largest potential savings from verification |

Aluminium | High — complex good | High (confirmed for UK CBAM; EU-specific figure to be checked) | Highest | High — verified data typically produces lower liability under UK CBAM |

Cement | Moderate | Present but not yet quantified | Medium | Not yet quantified — pending sector-specific data |

Fertilisers | Moderate | Present, mark-up mechanism applies | Medium | Moderate — verification value follows the standard mechanism |

Hydrogen | Emerging | Default-biased pending finalised methodology | Medium, rising | Not yet quantified — pending sector-specific data |

Electricity | Emerging | Defaults mandatory absent justified actual data | Lower, structurally | Not yet quantified — pending sector-specific data |

Table 9 — Supplier Risk Prioritisation Matrix

Sector | High Priority | Medium Priority | Lower Priority |

Steel | Suppliers with no verified upstream data | Partially verified suppliers | Fully verified suppliers |

Aluminium | Smelters with no verified emissions data | Partially documented suppliers | Fully verified smelters |

Cement, Fertilisers, Hydrogen, Electricity | To be prioritised once sector-specific figures are confirmed | — | — |

Framework — Sector Prioritisation Pyramid

Highest financial priority → Steel → Aluminium → Cement → Fertilisers → Hydrogen → Electricity

SECTION 7 — Practical Action Framework

Compliance Manager Decision Framework

This section converts the legal and financial analysis above into an operating sequence. It assumes the governance ownership set out in Section 3.

Step 1 — Identify High-Risk Imports (Owner: Compliance, with Procurement) Map imports by CN code and origin country against the sector risk ordering in Section 6. Cross-reference against supplier maturity and historical reporting quality — a supplier that has never provided emissions data before is a higher near-term default-value risk than one with an existing reporting relationship, regardless of sector.

Step 2 — Request Verified Emissions (Owner: Procurement) Issue a standard supplier questionnaire with a defined verification timetable and documentation checklist attached. This step should begin well ahead of the annual 31 May surrender deadline, given that verification by an accredited party under Article 8 and Annex VI is not instantaneous.

Step 3 — Evaluate Data Quality (Owner: Sustainability, with Compliance sign-off) Apply a defined accept/reject/clarify/default decision: accept where verified and complete; reject where implausible or unverifiable; request clarification where partial; fall back to default values only where none of the above resolves in time for the declaration.

Step 4 — Estimate Financial Exposure (Owner: Finance) Calculate embedded emissions and resulting certificate requirements for both the verified-data and default-value scenarios where a choice exists, using the current EU ETS price as the cost multiplier, so that the decision in Step 3 is made with the cost differential visible.

Step 5 — Governance Approval (Owner: Compliance, Procurement, Finance, Sustainability, Internal Audit) Any declaration relying on default values should pass through the internal approval chain set out in Section 3, with Internal Audit specifically confirming the evidence trail supporting the "actual data unavailable" determination.

Step 6 — Submit Declaration (Owner: Compliance) File the CBAM declaration under Article 6, citing the correct default-value implementing-regulation reference where applicable, and maintain the CBAM Registry record under Article 14 with full supporting documentation retained for audit.

Table 10 — Compliance Manager Checklist

Task | Owner | Deadline | Completed |

Map high-risk imports by CN code, origin, sector | Compliance | Start of reporting cycle | ☐ |

Issue supplier verified-emissions requests | Procurement | Well ahead of 31 May surrender deadline | ☐ |

Evaluate returned supplier data | Sustainability | Per supplier response | ☐ |

Model financial exposure, verified vs default | Finance | Before declaration decision | ☐ |

Obtain governance approval for any default-value use | Compliance, Procurement, Finance, Sustainability, Internal Audit | Before declaration submission | ☐ |

Submit CBAM declaration with correct citations | Compliance | By statutory deadline | ☐ |

Table 11 — Supplier Documentation Checklist

Document | Mandatory | Optional | Evidence Required |

Verified installation-specific emissions data | Where actual data is used | — | Accredited verifier confirmation (Article 8, Annex VI) |

Default-value implementing-regulation citation | Where a default is used | — | Reference to Implementing Regulation (EU) 2025/2621 provision applied |

Supplier questionnaire response | Yes, as part of engagement process | — | Retained for governance and audit review |

Verifier accreditation confirmation | Where verified data is submitted | — | Confirmation of EU accreditation status |

Framework — Supplier Decision Tree

Supplier provides verified emissions? → Yes: verify → submit → No: can acceptable evidence still be obtained? → Yes: verify → No: use Commission default values → estimate additional certificate cost → escalate supplier review

SECTION 8 — Strategic Outlook (2026–2027)

What Happens Next?

Default values are not a fixed feature of the definitive regime. The general pattern in EU carbon-pricing instruments is periodic review and revision as better data becomes available, and the same directional expectation applies to CBAM default values under 2025/2621, though no specific published review schedule or date is confirmed at the time of writing; any forward-looking date should be treated as inference pending confirmation.

Regulatory Outlook

The definitive regime is operational now, with the 31 May annual surrender cycle recurring going forward, and the Commission's default-values instrument governing every declaration relying on defaults from 1 January 2026 onward.

Expectations of further implementation refinements, benchmark revisions, or CBAM scope expansion are reasonable inferences from the general trajectory of EU carbon policy rather than confirmed regulatory developments, and are presented here as strategic judgement rather than fact.

Procurement Outlook

The structural incentive described in Section 2 — defaults priced above verified actuals — creates standing commercial pressure on overseas suppliers to improve their emissions reporting maturity over time, since suppliers unable to provide verified data become a source of avoidable cost for their EU buyers.

This dynamic reflects supplier engagement as a live commercial issue rather than a static compliance requirement; specific projections of supplier reporting-maturity timelines are not yet evidenced and are not offered here.

UK CBAM Trajectory

UK CBAM launches 1 January 2027, with HMRC's compliance-readiness workstream running through 2026 covering registration, thresholds, emissions methodology and the default-values concept. Unlike the EU, the UK has not yet published a consolidated implementing regulation equivalent to 2025/2621; its default-values and verification framework remains in guidance form.

Importers should not assume the UK will mirror the EU's specific mark-up methodology or figures once finalised — the conceptual logic is confirmed, but the numbers are not yet set.

Table 12 — Expected Regulatory Timeline

Year | Expected Development | Business Impact |

2026 | EU definitive regime fully operational; HMRC UK CBAM readiness workstream continues | EU certificate liability active now; UK planning window narrows |

2027 | UK CBAM launches (1 January); first full EU definitive-regime annual cycle completes (31 May surrender) | UK importers face first liability; EU importers complete first full-year reconciliation |

2028 and beyond | Not yet confirmed — monitor Commission and HMRC publications | To be updated once further guidance is published |

Framework — Future Readiness Roadmap

2026 (EU live, UK preparation) → 2027 (UK launch, first EU full-cycle surrender) → 2028+ (to be confirmed via ongoing monitoring)

The action for a Compliance Manager reading this report today is not to wait for that further guidance: begin supplier verification requests for steel and aluminium immediately, ahead of the next 31 May surrender deadline, since that is the one date in this timeline already confirmed and already running.

SECTION 9 — Frequently Asked Questions

When am I legally allowed to use EU CBAM default values instead of verified emissions?

Default values may be used only where actual installation-specific data is not available, under Article 7(2)(a) and Annex IV of Regulation (EU) 2023/956. It is not a standing election available whenever verified data would simply be more effort to obtain — the declaration must specify the default value used and its implementing-regulation reference under Article 6.

How much more could default values increase my CBAM certificate costs?

Default values under Implementing Regulation (EU) 2025/2621 include a mark-up over best-available data, which increases the embedded-emissions figure and therefore the certificate obligation calculated against the EU ETS price. The specific percentage mark-up by product and country is published in the Regulation's annexes and should be checked directly for any given import.

Can I replace default values with verified emissions before submitting my annual CBAM declaration?

Yes in principle. Verified emissions are the preferred methodology under Article 7(2)(a), and a default should only be used where actual data genuinely cannot be obtained in time. The practical constraint is timing: verification by an accredited party under Article 8 and Annex VI takes time, so supplier engagement needs to begin well ahead of the 31 May surrender deadline.

Which CBAM sectors are most affected by default values?

Steel and aluminium carry the highest documented exposure, both being treated as complex goods requiring upstream verification; the UK CBAM aluminium finding specifically confirms verified actuals produce a lower liability than defaults. Cement, fertilisers, hydrogen and electricity are subject to the same mechanism, though sector-specific figures for those four are not yet published.

What evidence should I keep if regulators question my use of default values?

Retain documentation showing that actual data was genuinely unavailable at the time of declaration, the specific default value and implementing-regulation reference applied, and internal governance sign-off from Compliance, Finance, Procurement, Sustainability and Internal Audit.

What should I do if my overseas supplier cannot provide verified emissions data?

Escalate through the supplier decision tree in Section 7: confirm whether any acceptable partial evidence exists before falling back to Commission default values, and treat repeated inability to supply verified data as a factor in future supplier and procurement decisions given the direct cost consequence of defaulting.

SECTION 10 — References & Sources

The report is supported by a comprehensive range of primary legislation, implementing regulations, official European Commission guidance, industry publications, and technical references to ensure regulatory accuracy and practical relevance.

Primary Legislation

Regulation (EU) 2023/956 (EU CBAM Regulation) — Core legal framework governing the EU Carbon Border Adjustment Mechanism, including Articles 6, 7(2)(a), 8, and 14, together with Annexes IV and VI, covering CBAM declarations, the use of actual and default emissions, verification requirements, and the CBAM Registry.

Implementing Regulations

Commission Implementing Regulation (EU) 2025/2621 — Establishes the methodology and country- and product-specific default values applicable under the EU CBAM definitive regime.

Commission Implementing Regulation (EU) 2023/1773 — Sets out the reporting rules and procedures applicable during the EU CBAM transitional period.

European Commission Guidance

European Commission, Default Values for the Transitional Period (22 December 2023).

European Commission (Taxation and Customs Union), CBAM Legislation and Guidance Portal.

European Commission (Taxation and Customs Union), Carbon Border Adjustment Mechanism Overview.

European Commission (Climate Action), CBAM Overview Document (January 2023).

National Competent Authorities

HMRC UK CBAM Guidance (referenced through CBAM Journal reporting), covering importer registration requirements, reporting thresholds, emissions methodology, and the use of default values under the forthcoming UK CBAM regime.

Industry Guidance

Climate Leadership Council, A Guide to the EU CBAM (April 2026).

Carbon Chain, CBAM: Your Guide to the EU Carbon Border Adjustment Mechanism.

Solidwaretools, CBAM Default Values by Country technical resource.

Technical References

EY, European Commission Publishes "Default Values" for the CBAM Transitional Period (3 May 2026).

CBAM Journal research articles, including:

UK CBAM for Aluminium Importers (29 June 2026).

What Is Embedded Carbon Under UK CBAM? (1 July 2026).

A Compliance Manager's Guide to HMRC Registration, Threshold and Compliance (8 June 2026).

15 Critical Differences Importers Must Understand Before 2027 (7 June 2026).

EU CBAM Definitive Regime 2026 (28 May 2026).

Legal Disclaimer:

This report is published by CBAM Journal, an independent research publication operated by Sekason Research Limited (London), and is provided solely for informational and regulatory intelligence purposes. It does not constitute legal, tax, accounting, financial, or professional advice, nor should it be relied upon as a substitute for advice from qualified legal, tax, customs, or compliance professionals.

While every effort has been made to ensure the accuracy of the information at the time of publication, EU and UK CBAM legislation, implementing regulations, guidance, carbon prices, and administrative requirements may change without notice. Readers are responsible for verifying all regulatory obligations, calculations, and reporting requirements against the latest official legislation and guidance issued by the European Commission, HMRC, and other competent authorities before submitting any CBAM declaration or making compliance decisions.

Neither Sekason Research Limited nor CBAM Journal accepts any liability for any loss, damage, or consequences arising from the use of, or reliance on, the information contained in this report.

For the complete legal disclaimer, please visit: https://www.cbamjournal.com/legal-disclaimer.

Comments