EU CBAM Certificates Explained: How the Cost Is Calculated

- Ahtesham Shaikh

- Jun 23

- 14 min read

Updated: Jun 26

What EU CBAM Certificates Are and Why They Exist

The EU Carbon Border Adjustment Mechanism operates on a straightforward regulatory logic: goods produced outside the European Union and imported into EU territory should carry the same carbon cost as equivalent goods manufactured inside the EU under the EU Emissions Trading System. Without this equivalence, EU producers paying for their carbon emissions face a structural cost disadvantage against importers from jurisdictions with weaker or no carbon pricing. CBAM closes that gap.

The instrument through which this carbon cost is applied to imports is the CBAM certificate. Every authorised CBAM declarant — the entity registered with national competent authorities to import CBAM goods — is required to purchase these certificates and surrender them annually in proportion to the verified embedded emissions in the goods they have imported.

A CBAM certificate is not a customs duty. It is not a tariff. It is a carbon price mechanism, and its cost is directly tied to the carbon intensity of the imported goods and the prevailing price of carbon in the EU ETS.

Understanding how certificates are priced, how many must be surrendered, and what the consequences of non-compliance look like is not optional for businesses importing steel, aluminium, cement, fertilisers, hydrogen, or electricity into the EU.

From 1 January 2026, the EU CBAM is in its definitive phase. Obligations are live. The certificate system is operational under the enforceable legal framework set out in Regulation (EU) 2023/956, as amended by Regulation (EU) 2025/2083.

Who Must Deal With CBAM Certificates

Before reaching the certificate mechanics, the threshold question matters. Under the Simplification Regulation (EU) 2025/2083, which took effect on 20 October 2025, a single mass-based threshold now applies: importers bringing in 50 tonnes or less of CBAM-covered goods per calendar year are exempt from authorisation, declaration, and certificate surrender obligations. This replaced the previous €150 per consignment de minimis threshold, which the Commission considered insufficient to reflect actual emissions impact.

Electricity and hydrogen are excluded from this mass-based threshold exemption and remain in scope regardless of import volume.

Where the 50-tonne threshold is exceeded, the obligations apply to the totality of imports for that calendar year — including quantities imported before the threshold was crossed. There is no partial-year relief.

The entity responsible for certificate obligations is the authorised CBAM declarant — the EU importer of record, or their indirect customs representative where applicable. Authorisation must be obtained from the competent national authority in the member state of establishment before imports of CBAM goods commence above the threshold. Declarants who submitted applications by 31 March 2026 were permitted to continue importing provisionally pending a decision on their application.

The Regulatory Framework Governing Certificate Pricing

The legal basis for EU CBAM certificates sits in Regulation (EU) 2023/956, the founding CBAM regulation adopted by the European Parliament and Council in May 2023. The pricing methodology is governed by Commission Implementing Regulation (EU) 2025/2548, adopted on 10 December 2025, which specifies precisely how certificate prices are calculated and published.

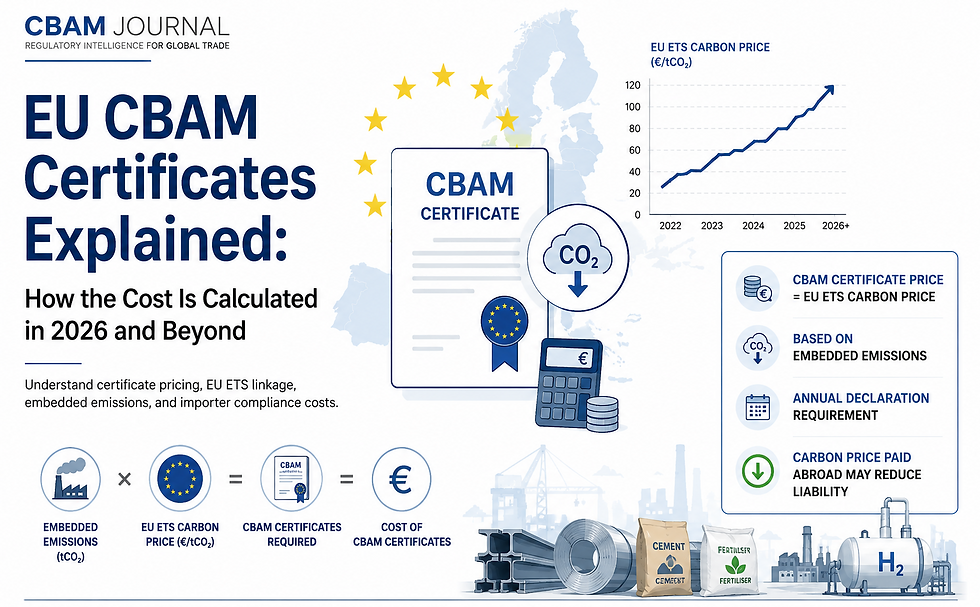

The methodology is designed to ensure that the certificate price mirrors the carbon cost paid by EU producers under the EU ETS. The Commission calculates certificate prices as the weighted average of EU ETS allowance auction clearing prices — the prices at which successful bidders purchase allowances in authorised auctions — over the relevant reference period.

For 2026 imports, the price is set on a quarterly basis: one price per calendar quarter, calculated by the Commission during the first week of the following quarter and published on the Commission's website and in the CBAM Registry. In 2026, the Commission calculates and publishes four quarterly prices, one for each calendar quarter. The first quarterly certificate price, covering Q1 2026 imports, was approximately €75.36 per tonne CO₂e, published on 7 April 2026. European CommissionCBAM Journal

From 1 January 2027, the pricing cadence shifts to a weekly basis: from 2027, the certificate price mirrors the weekly average price of EU ETS allowances. Mayer Brown

The EU ETS auction price itself is not fixed. It reflects supply and demand dynamics in the carbon allowance market, influenced by the EU's overall emissions cap, economic activity, energy market conditions, and the ongoing tightening of the cap under the Fit for 55 legislative package. Certificate cost is therefore variable by design. A declarant importing throughout 2026 will face different certificate prices for Q1, Q2, Q3, and Q4 imports.

There is no secondary market for CBAM certificates. They cannot be traded between declarants. They may only be purchased from the CBAM Registry and, under specific conditions, resold back to competent authorities.

How the Certificate Price Is Calculated in Practice

The cost of the certificate obligation for any given import flows from three variables:

Variable | Description |

Quantity of goods imported | Tonnes, disaggregated by commodity type and CN code |

Embedded emissions intensity | Tonnes of CO₂e per tonne of product (actual or default) |

Applicable certificate price | € per tCO₂e for the relevant quarter (2026) or week (2027+) |

The calculation is:

Certificates to surrender = Embedded emissions intensity (tCO₂e/t) × Quantity imported (tonnes)

Certificate cost = Certificates to surrender × Certificate price (€/tCO₂e)

A practical illustration: a declarant importing 1,000 tonnes of hot-rolled coil steel with a verified embedded emissions intensity of 1.8 tCO₂e per tonne would need to surrender 1,800 certificates. At a certificate price of €75 per tonne of CO₂, the certificate cost for that import would be €135,000. Had the declarant relied on a default emissions value of 2.4 tCO₂e per tonne instead, the obligation would rise to 2,400 certificates and the cost to €180,000 — a €45,000 difference attributable solely to the emissions data source.

This illustrates why the question of how embedded emissions are calculated and verified is a direct financial question, not a secondary compliance matter.

What Counts as Embedded Emissions

The scope of embedded emissions that must be accounted for under EU CBAM varies by sector and is a consistent source of compliance error.

For most sectors — including steel, cement, fertilisers, and hydrogen — the obligation covers direct emissions: greenhouse gas emissions produced during the manufacturing process itself, including combustion of fuels, chemical reactions in production, and process-related releases at the installation where the goods are made.

For aluminium, Annex II of Regulation (EU) 2023/956 specifies that only direct emissions are in scope under the current framework. Indirect emissions — those associated with the electricity consumed during production — are excluded from the CBAM certificate obligation for aluminium imports.

This is a material distinction: aluminium smelting is highly electricity-intensive, and the carbon intensity of the supplying grid can be significant. For CBAM purposes, that indirect carbon cost does not currently generate a certificate obligation for aluminium imports.

For complex goods — those manufactured from other goods that are themselves CBAM-covered — the embedded emissions calculation must account for emissions embedded in the precursor materials as well as the direct emissions of the final manufacturing process. A steel pipe carries the embedded emissions of the steel from which it was made, plus the direct emissions of the pipe-manufacturing process. This layered calculation places significant demands on supply chain data and is a frequent source of under-reporting.

For electricity imported directly into the EU, a different methodology applies, reflecting the nature of electricity as a product with no conventional physical mass.

The European Commission has published default values for all CBAM-covered goods, differentiated by country of origin and product type. Most newly established default values will rise by 10% in 2026, 20% in 2027, and 30% from 2028 onwards — a built-in financial incentive for declarants to obtain and use verified actual emissions data rather than default figures. Icapcarbonaction

The Surrender Obligation: Timing, Quantity, and the Registry

The surrender of CBAM certificates follows a defined annual timeline that has been updated under the Simplification Regulation.

The key dates are:

Obligation | Deadline |

Certificate purchase opens for 2026 imports | 1 February 2027 |

Annual CBAM declaration submission | 30 September of the year following importation |

Certificate surrender | 30 September of the year following importation |

Quarterly holding requirement (end of each quarter) | 50% of embedded emissions from imports year-to-date |

Cancellation of unsurrendered prior-year certificates | 1 July each year |

The 30 September deadline — not 31 May as set out in the original Regulation (EU) 2023/956 — reflects the amendment made by Regulation (EU) 2025/2083. For 2026 imports, the first annual declaration and certificate surrender is therefore due by 30 September 2027.

The annual declaration must state: total quantities of each CBAM good imported, verified embedded emissions, any carbon price paid in the country of origin, and the number of certificates being surrendered. The declaration must be verified by an accredited verifier — an independent third party accredited by a national accreditation body in an EU member state. Self-certification is not permitted for declarations using actual emissions data.

The quarterly holding requirement stands at 50% of cumulative embedded emissions from the start of the calendar year, assessed at the end of each quarter. This is an in-year liquidity obligation. The minimum quarterly purchase requirement for CBAM certificates is reduced to 50% of embedded emissions in all CBAM goods imported since the beginning of the calendar year, with adjustments for free allocation. A declarant who imports heavily in Q1 but purchases no certificates until September faces a technical breach even if they ultimately surrender the correct number of certificates before the annual deadline. Mayer Brown

Excess certificates held after the surrender date may be resold back to the competent national authority at the purchase price. All certificates purchased in the calendar year before last and still held in declarant accounts are cancelled without compensation by the Commission on 1 July of each year.

The Free Allocation Adjustment

One provision that reduces the certificate obligation — but which is not straightforward to apply — is the free allocation adjustment. During the phase-out of free EU ETS allowances for CBAM-covered sectors (running from 2026 to 2034), CBAM declarants are not required to surrender certificates for the proportion of embedded emissions that corresponds to free allowances still being granted to EU producers in the same sector.

This adjustment is calculated using a CBAM factor published by the Commission, which reflects the share of production not covered by free allocations for each sector. For 2026 and 2027, free allocations of EU ETS allowances for eligible producers in CBAM-covered sectors are reduced by 2.5% annually. As free allocations are phased out, the CBAM factor increases, and the certificate surrender obligation rises proportionally. Icapcarbonaction

The practical effect for 2026 is that the certificate surrender obligation is somewhat lower than it will be once free allocations are fully phased out. Declarants should not treat current-year certificate costs as representative of their long-term CBAM exposure.

Carbon Price Deductions: Reducing the Certificate Obligation

Where a verified carbon price has been paid in the country of origin — through an emissions trading scheme, a carbon tax, or an equivalent mechanism — the declarant may reduce their certificate surrender obligation by the carbon cost already paid. The logic is to avoid double carbon pricing on the same tonne of emissions.

This deduction is not automatic. It requires:

Documentary evidence of the carbon price paid

Verification against Commission guidance on qualifying third-country carbon pricing schemes

Accurate currency conversion to euros

Application through the annual declaration process

The Commission is developing implementing legislation specifying which third-country carbon pricing schemes qualify and how actual payments are converted into a certificate reduction. A call for evidence was launched on 28 August 2025 to gather stakeholder views on the rules for deducting carbon prices paid in third countries. Until that implementing act is finalised, the deduction mechanism carries operational uncertainty for declarants from countries with existing carbon pricing schemes. European Commission

In practice, the deduction is most relevant for imports from jurisdictions operating credible carbon pricing at or approaching EU ETS levels. For imports from countries with no carbon price or a carbon price substantially below the EU ETS level, the full certificate obligation applies.

What Happens If You Get It Wrong: The Penalty Framework

Authorised declarants who fail to surrender sufficient certificates face a penalty of €100 per tonne of CO₂, indexed to the European inflation rate. Paying the fine does not exempt the declarant from the obligation to surrender the missing certificates. Anthesis Global

The penalty framework operates as follows:

Non-compliance Type | Penalty |

Failure to surrender sufficient certificates (authorised declarant) | €100 per tonne CO₂e of shortfall, inflation-indexed |

Importing CBAM goods without authorised declarant status | 3 to 5 times the standard €100 penalty per tonne |

Failure to meet quarterly 50% holding requirement | National competent authority enforcement action |

Inaccurate or missing annual declaration | Commission assessment and penalty proceedings |

Two consequences compound the financial impact of under-surrender. First, the payment of the penalty does not release the authorised CBAM declarant from the obligation to surrender the outstanding number of CBAM certificates. The declarant owes both the penalty and the certificates. Second, if an importer exceeds the single mass-based threshold without authorised CBAM declarant status, penalties apply amounting to three to five times the standard penalty of €100 per tonne of embedded emissions. EUR-LexMayer Brown

At a certificate price in the range of €60–€80 per tonne, the €100 penalty per tonne of shortfall represents a surcharge of 25% to 67% above the underlying certificate cost. For a declarant with a material under-surrender — say 5,000 certificates — the penalty alone could reach €500,000, with the certificate purchase obligation still outstanding.

Persistent non-compliance carries the additional risk of suspension of authorised declarant status, which would prevent the entity from importing CBAM goods into the EU.

Common Sources of Certificate Miscalculation

The gap between the certificate obligation a declarant anticipates and the obligation confirmed by a verified declaration is frequently larger than expected.

The sources of divergence are consistent across sectors.

Unverified supplier data is the most common driver. A supplier may provide emissions intensity figures reflecting best-case production conditions or an earlier reporting period. Without independent verification by an accredited verifier, those figures cannot be used in the annual declaration. Declarants who build cost models on unverified data regularly find figures revised upward through the verification process.

Mishandling of complex goods causes systematic under-reporting. Declarants importing manufactured goods that incorporate CBAM-covered inputs often track only the direct emissions of the final manufacturing step, omitting the embedded emissions of precursor materials. The obligation covers both.

Commodity code misclassification distorts the calculation at source. EU CBAM applies to specific goods defined by CN codes in Annex I of Regulation (EU) 2023/956. Misidentifying a product under an incorrect code produces a certificate calculation based on the wrong emissions parameters.

Quarterly holding shortfalls are an operational risk that is easy to underestimate. Declarants focused on the annual 30 September deadline and inattentive to the quarterly 50% holding requirement may be technically non-compliant even if they ultimately surrender the correct number of certificates at year end.

Currency conversion errors in calculating origin-country carbon price deductions — particularly where exchange rate movements between the payment date and the conversion date are not tracked correctly — produce deduction figures that differ from those a verifier will accept.

Practical Preparation: What Declarants Need in Place

The certificate obligation is not manageable without advance preparation. The data requirements, verification requirements, and registry mechanics all carry lead times that make last-minute compliance structurally difficult.

Registry access must be established before CBAM goods are imported above the 50-tonne threshold. Authorised declarant status is granted by the competent national authority. Processing timelines vary by member state.

Supplier engagement on emissions data must begin well ahead of the declaration period. Collecting, validating, and submitting actual emissions data to an accredited verifier is a process with significant lead time. Declarants who have not begun supplier data collection by mid-year face a high risk of defaulting to default values — and the associated higher certificate costs from 2026 onwards as default values escalate.

Accredited verifier selection should be completed early. The number of accredited verifiers across EU member states remains limited relative to the scale of CBAM-affected import volumes. Verifiers in high-demand sectors such as steel and aluminium are likely to be committed during peak declaration periods approaching the September deadline.

Cost modelling should be built around scenarios, not single-point estimates. Certificate prices will vary quarterly in 2026 and weekly from 2027. Verified emissions data may differ from initial supplier figures. Origin-country carbon price deductions depend on implementing legislation not yet finalised. A model built on fixed assumptions will diverge from actual exposure.

Cash flow planning must reflect the quarterly 50% holding requirement, not just the annual surrender deadline. Certificate purchase costs begin accumulating from the point imports commence, not as a single payment in September.

The Sourcing Implication: Certificate Cost as a Procurement Variable

The CBAM certificate obligation is not cost-neutral across sourcing geographies and supplier types. It introduces a direct financial differential between suppliers based on their emissions intensity and the carbon pricing regime of their home jurisdiction.

A supplier operating modern electric arc furnace steelmaking with verified low embedded emissions generates a substantially lower certificate obligation than a supplier operating coal-fuelled blast furnace production. That differential flows directly through the certificate cost calculation and is quantifiable at the procurement stage.

The origin-country carbon price deduction creates a further geographic differential: equivalent goods produced in jurisdictions with credible carbon pricing at or near EU ETS levels carry lower net CBAM costs for EU importers than goods from countries with no carbon price. The UK, operating its own UK ETS, is a relevant example — though the deduction mechanics for UK-origin goods depend on implementing legislation currently being finalised.

For procurement and supply chain teams, CBAM certificate cost is now a quantifiable input into total landed cost calculations alongside freight, tariffs, and insurance. Procurement decisions made without integrating CBAM certificate cost are made on an incomplete financial basis.

What Changes From 2027

The shift from quarterly to weekly certificate pricing from 1 January 2027 has operational implications for declarants managing certificate purchases through the year.

Weekly pricing means that the price at which certificates are purchased will vary more frequently, reflecting EU ETS movements from week to week. Declarants accumulating certificates across the year will hold a portfolio purchased at different weekly prices. Finance teams will need processes to monitor weekly published prices and incorporate them into certificate purchase planning and cost forecasting.

The weekly pricing data is published by the European Commission and will be made available in declarant accounts in the CBAM Registry. Declarants should confirm with their registry administrator how price notifications will be delivered to ensure they are acting on current figures rather than cached data.

Frequently Asked Questions

What is the current price of an EU CBAM certificate?

Certificate prices are set quarterly in 2026 as the weighted average of EU ETS allowance auction clearing prices. The Q1 2026 price was approximately €75.36 per tonne CO₂e, published on 7 April 2026. Subsequent quarterly prices are published in the first week following each quarter end. From 2027, prices are set and published weekly. Current prices are available at the European Commission's CBAM portal and in declarant registry accounts.

When do I need to purchase and surrender CBAM certificates for my 2026 imports?

Certificate purchase for 2026 imports opens on 1 February 2027. The annual CBAM declaration and certificate surrender deadline for 2026 imports is 30 September 2027. However, the in-year quarterly holding requirement — 50% of cumulative embedded emissions — applies from the moment imports commence, assessed at each quarter end.

Can I use my supplier's emissions figures without verification?

Default values may be used without verification. Actual emissions data from suppliers requires verification by an accredited verifier before it can be used in an annual CBAM declaration. Unverified supplier-provided figures cannot be submitted as actual emissions data. Given that default values are calibrated conservatively and are set to escalate in 2027 and 2028, obtaining verified actual data is financially advantageous for most declarants importing from modern, well-managed production facilities.

What happens if I under-surrender certificates?

A penalty of €100 per tonne of CO₂e for each certificate not surrendered applies, indexed to the European inflation rate. Paying the penalty does not extinguish the obligation — the missing certificates must still be surrendered. The total cost of an under-surrender is therefore the penalty plus the certificate purchase cost.

Does the carbon price my supplier paid in their home country reduce my CBAM certificate obligation?Yes, in principle. Where a verified carbon price has been paid in the country of origin, the declarant can claim a reduction in certificates to surrender. The implementing legislation specifying which third-country schemes qualify and the exact deduction methodology is being finalised by the Commission. Until it is in force, the practical application of this deduction carries some procedural uncertainty.

Am I in scope if I import less than 50 tonnes of CBAM goods per year?

No. Under Regulation (EU) 2025/2083, importers whose total annual imports of CBAM-covered goods remain at or below 50 tonnes (cumulative net mass) are exempt from all CBAM obligations, including authorisation, declaration, and certificate surrender. Note that electricity and hydrogen are excluded from this exemption. If imports exceed 50 tonnes in any calendar year, all imports for that year — including those below the threshold — become subject to the full obligation.

References and Sources

This article is backed by authoritative source and research;

European Commission – Carbon Border Adjustment Mechanism — Price of CBAM Certificates

URL: taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism/price-cbam-certificates_en

EUR-Lex – Regulation (EU) 2023/956 of the European Parliament and of the Council (Consolidated Version)

EUR-Lex – Commission Implementing Regulation (EU) 2025/2548 of 10 December 2025

URL: eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32025R2548

EUR-Lex – Regulation (EU) 2025/2083 — CBAM Simplification Regulation (17 October 2025)

URL: eur-lex.europa.eu

European Commission – Carbon Border Adjustment Mechanism — Main Portal

URL: taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en

ICAP (International Carbon Action Partnership) – EU CBAM Enters Compliance Phase and Outlines Path Ahead

URL: icapcarbonaction.com

ICAP (International Carbon Action Partnership) – EU Adopts Simplifications of CBAM Rules Ahead of Compliance Phase

URL: icapcarbonaction.com

Mayer Brown – EU Adopts CBAM Simplification Regulation: 10 Key Amendments

URL: mayerbrown.com

DEHSt (German Emissions Trading Authority) – CBAM Certificates — Definitive Regime 2026

URL: dehst.de

CBAM Journal – EU CBAM Definitive Regime 2026

URL: cbamjournal.com

Legal Disclaimer

This article is published by CBAM Journal, operated by Sekason Research Limited, London. It is provided for informational and intelligence purposes only and does not constitute legal, financial, or regulatory advice. Readers should seek independent professional advice specific to their circumstances. Regulatory details reflect the position as of the date of publication. Readers should verify current obligations against European Commission guidance and official EU legislation before making compliance decisions. CBAM Journal is not affiliated with the European Commission, HMRC, or any regulatory authority. Read complete disclaimer; https://www.cbamjournal.com/disclaimer

Comments